PwC: Below inflationary growth in RevPAR plagues US lodging industry

Third quarter results continued to disappoint - once again coming in below expectations, with RevPAR growth of just 0.7 percent. Lodging supply growth outpaced demand in the quarter, resulting in a 0.1 percent decline in occupancy levels. A slight increase in transient demand failed to off-set declines in the group and contract segments.

While RevPAR increased during the quarter, it was the lowest year- over-year growth since the beginning of the US lodging industry's recovery from the Great Recession, and the only quarter in the current lodging cycle with a RevPAR increase below 1.0 percent. Although US hotels have experienced RevPAR increases in 112 of the last 115 months, growth continues to decelerate, with two of the three declines coming in June and September of this year. Looking ahead to the final quarter of 2019, the near-term lodging outlook suggests continued deceleration in top line metrics. Weak demand and a general lack of pricing power in October supports this outlook.

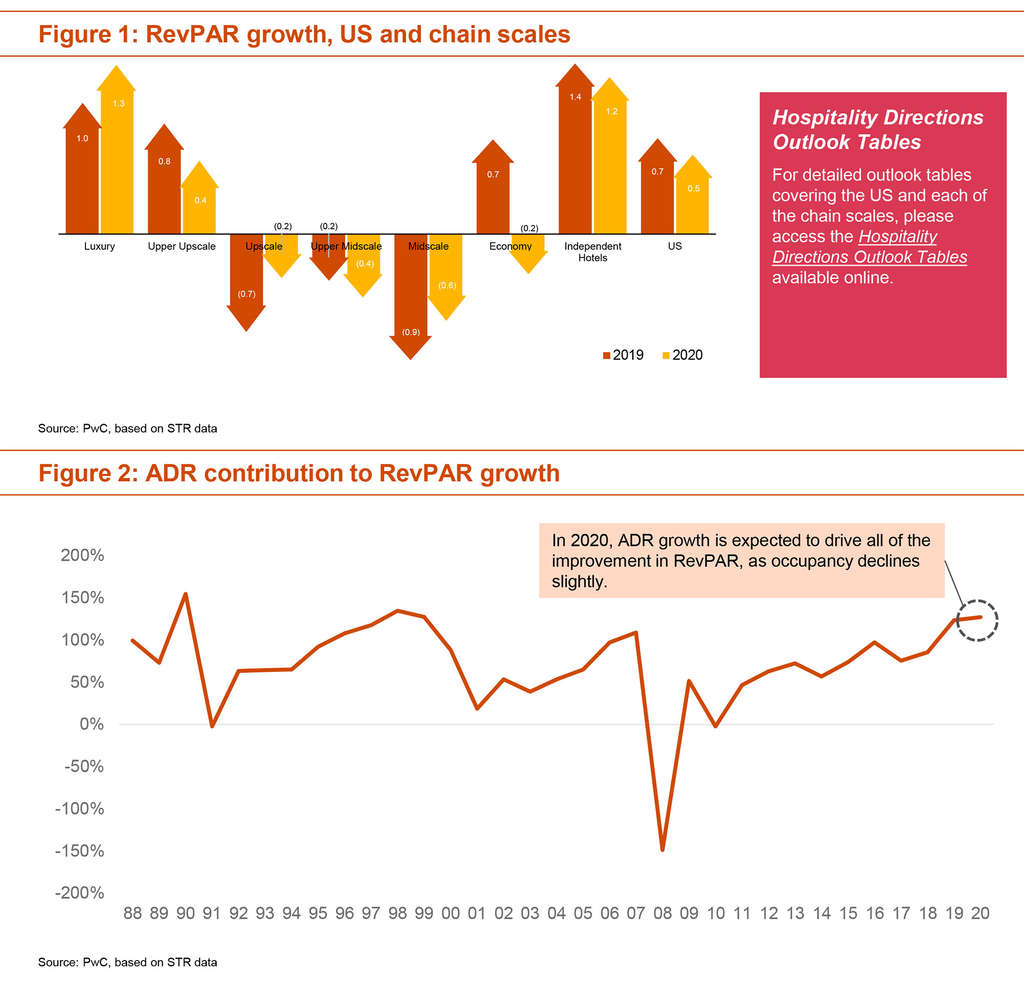

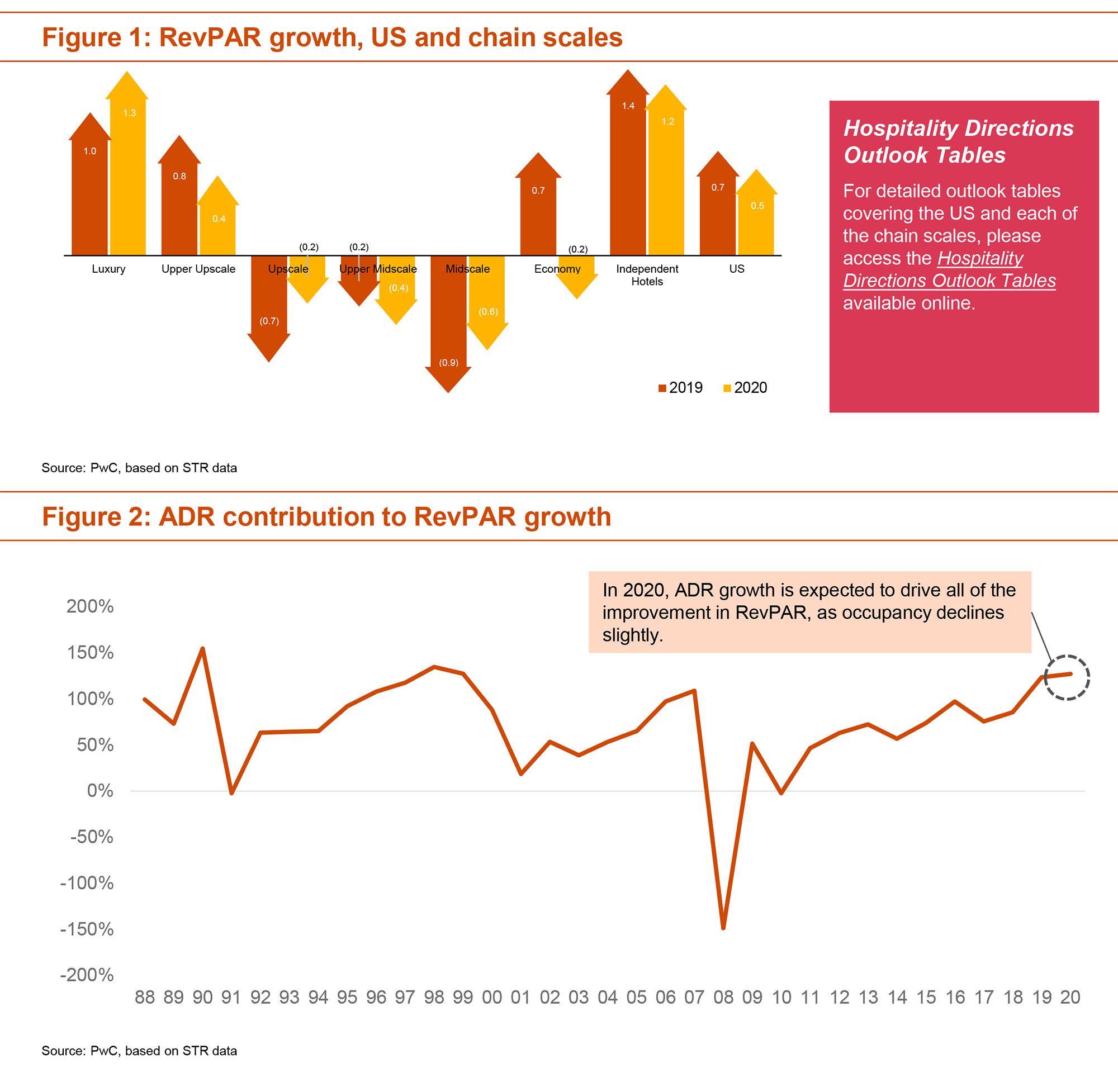

In 2020, despite an expected boost to lodging demand from the upcoming presidential election, supply is expected to exceed demand growth, resulting in a minor decrease in occupancy levels. Rising inflation is expected to help support what is still expected to be decelerating ADR growth, resulting in a marginal RevPAR increase of 0.5 percent. Challenges to the above outlook include tempered investor confidence and political uncertainty both domestically and abroad, leading up to the presidential election.

About PwC US

PwC US helps organizations and individuals create the value they're looking for. We're a member of the PwC network of firms in 157 countries with more than 195,000 people. We're committed to delivering quality in assurance, tax and advisory services. Tell us what matters to you and find out more by visiting us at www.pwc.com/US. PwC refers to the US member firm, and may sometimes refer to the PwC network. Each member firm is a separate legal entity. Please see www.pwc.com/structure for further details.