CBRE 2025 U.S. Hotel Investor Intentions Survey

Optimism Increases Among Hotel Investors

The 2025 U.S. Hotel Investor Intentions Survey reveals growing optimism among investors driven by positive outlooks on returns and distressed opportunities.

Key Takeaways:

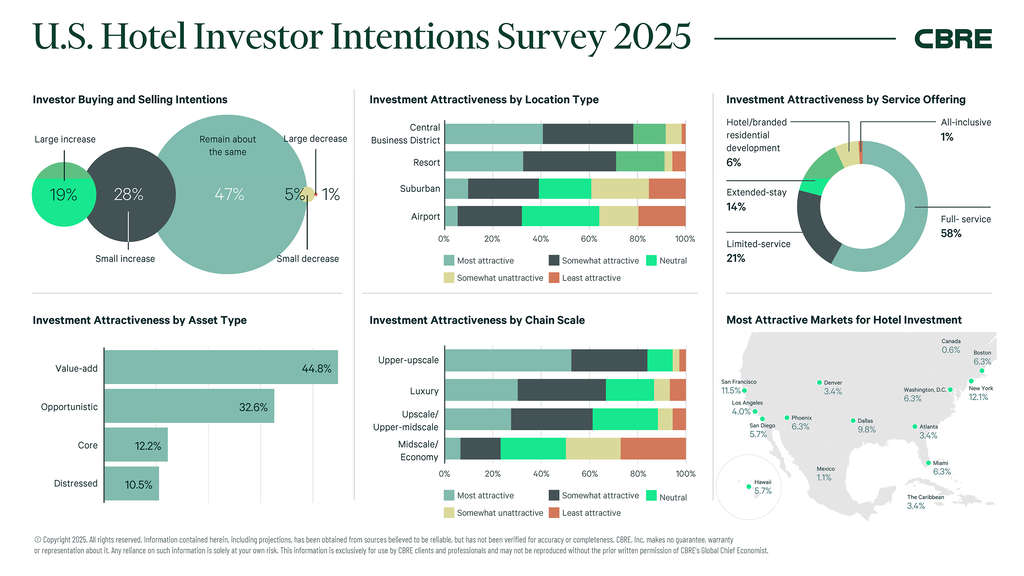

- Optimism among U.S. hotel investors is on the rise, with 94% planning to maintain or increase their investments in 2025, up from 85% in 2024.

- Central business districts (CBDs) and resorts are the most favored locations for investment.

- 77% of respondents targeted value-added and opportunistic hotel assets for investment.

- Labor, insurance, and capital costs remain significant concerns, though they are less severe than last year.

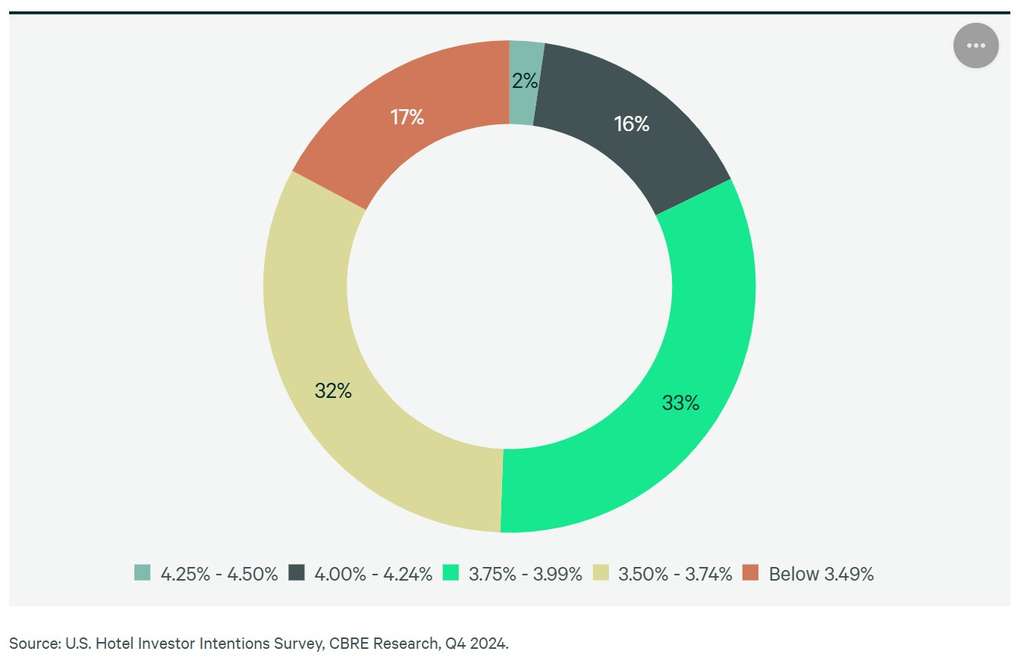

- Lowering the federal funds rate to at least 3.75% is seen as necessary to catalyze investment activity, with CBRE predicting a year-end rate of 3.5% to 3.75%.

- New York City remains the most attractive investment market for the second year, followed by San Francisco and Dallas.

- Full-service hotels are increasingly popular for acquisition or development, driven by the resurgence of business travel and return-to-office mandates.

Executive Summary

- Sentiment among U.S. hotel investors is increasingly positive, with 94% of those recently surveyed by CBRE expecting to maintain or increase their hotel investments in 2025, compared with 85% last year. A more optimistic outlook for total returns and distressed investment opportunities were the key reasons cited for increased allocations.

- The most favored location types in 2025 are central business districts (CBDs) and resorts, while higher-priced options are the most popular chain scales. We expect RevPAR growth of 2.2% for urban locations in 2025, driven by increased group, business transient and international travel. Leisure demand should continue to normalize, with modest ADR gains leading to 1.5% RevPAR growth for resort locations.

- Among investors who plan to decrease their capital allocations this year, decelerating RevPAR growth was cited as the biggest reason. Investors noted that labor, insurance and capital costs were still the primary concerns for 2025, but the severity of these challenges was less than it was last year.

- Investors indicated that lowering the federal funds rate to at least 3.75% this year will be needed to catalyze increased investment activity. CBRE expects the federal funds rate to close the year at a range of 3.5% to 3.75%.

- Given limited new hotel supply, short-term rental unit restrictions and strong consumer dynamics, New York City was cited as the most attractive investment market for the second consecutive year. San Francisco was second-most favored, followed by Dallas.

U.S. Hotel Investor Intentions Survey 2025

CBRE Hotels Research conducted its second annual U.S. Hotel Investor Intentions Survey in Q4 2024 to assess the climate and sentiment for hotel investment in 2025.

Almost all respondents (94%) expect hotel investment to remain the same or increase in 2025, up from 85% of respondents to our 2024 survey. Just 6% of respondents expect to decrease their hotel investments this year, compared with 16% in 2024.

Figure 1: Hotel Investment Activity Expectations, 2025 vs. 2024

Investors continue to favor value-add and opportunistic hotel investments, with 77% of respondents targeting these asset types in 2025 compared with 72% last year. We expect profits to remain relatively flat in 2025.

Only 11% of total survey respondents are targeting distressed assets this year, down from 18% last year despite 25% of those looking to increase their capital allocations to hotels citing distressed opportunities as the primary reason why.

Figure 2: Favored Asset Types in 2025 vs. 2024

Nineteen percent of respondents also cited more optimistic total return prospects as a key reason to increase their hotel allocations, while another 19% cited price adjustments.

Of those investors who expect to reduce their allocation to hotels, 25% cited declining RevPAR growth as the key reason. However, it’s possible that the recent reacceleration in RevPAR growth could lead to fewer dispositions than expected.

Figure 3: Reasons to Increase Hotel Allocations in 2025

Figure 4: Reasons to Decrease Hotel Allocations in 2025

Hotel investors appear to be slightly more interested in disposing hotels affiliated with globally recognized brands than they were last year (57% vs. 54%).

In a switch from 2024, investors appear more bullish on independent hotels, with 14% expecting to acquire them this year vs. 10% last year and just 7% expecting to dispose of them this year vs. 18% last year.

Figure 5: Most Likely Acquisition/Disposition Targets in 2025

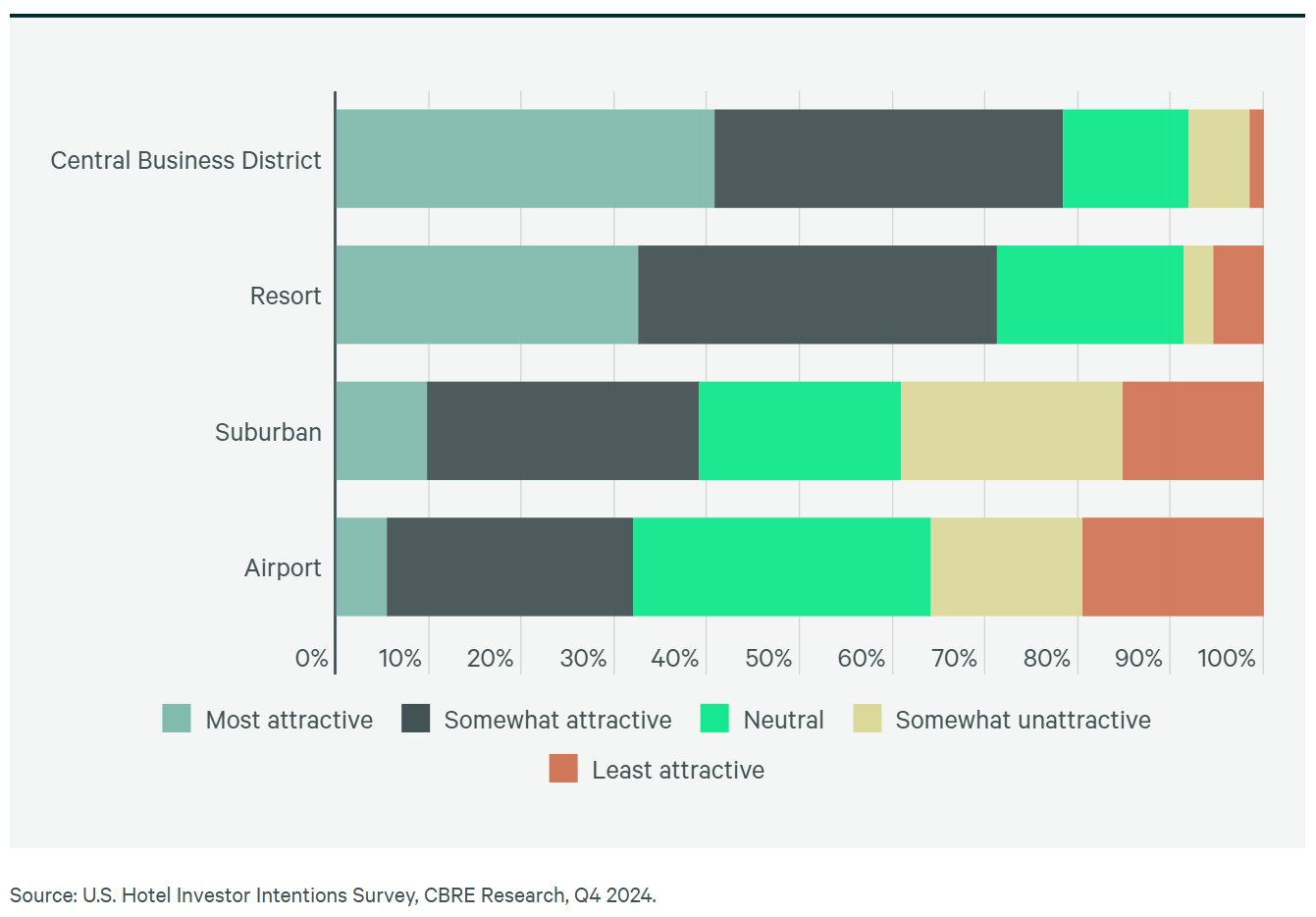

Resort & CBD Assets Remain Most Favored

Forty-one percent of survey respondents said that hotels in CBD locations are the most attractive for incremental investment, followed by 33% citing resort locations as most attractive.

Driven by the ongoing recovery in inbound international travel and continued improvement in meetings and group events, we expect RevPAR growth for urban locations to outperform in 2025. Airport and suburban assets are the least attractive, cited as such by 20% and 15% of respondents, respectively.

Figure 6: Ranking of Location Types for Incremental Investment

Investors Prefer Higher-Priced Chain Scales

Upper upscale hotels were cited as most attractive by 53% of surveyed investors, followed by 30% citing luxury hotels as most attractive.

This is a slight shift from last year when upper midscale was among the most attractive chain scales for investment. Continued weakness in RevPAR growth has increasingly led to midscale/economy hotels being the least appealing chain scale for incremental investment, cited as such by 27% of respondents.

Figure 7: Ranking of Chain Scales for Incremental Investment

Figure 8: Most/Somewhat Attractive Chain Scales, 2025 vs. 2024

Nearly 60% of survey respondents said full-service hotels are their most likely target for acquisition or development this year, compared with 20% in 2024, perhaps due to the resurgence of business transient and group travel and the rise in return-to-office mandates.

Investor interest in extended-stay assets remains modest, cited by only 14% of respondents as an acquisition target this year vs. 13% last year.

Figure 9: Acquisition/Development Targets by Property Type, 2025 vs. 2024

Margin pressures remain top of mind for respondents, with rising labor and capital costs cited as the most challenging issues in 2025. Investors appear more concerned about weakening demand this year than last, with 65% identifying this as an issue vs. 46% in 2024.

While investors remain concerned about capital costs, they appear less so than last year. The Fed has lowered the federal funds rate by 100 basis points (bps) since September 2024 and CBRE expects another 50 bps in cuts this year to a range of 3.5% to 3.75% by year-end. Survey respondents indicated that these levels are needed to kickstart investment activity.

Figure 10: Most Challenging Issues in 2025

Figure 11: Most/Somewhat Challenging Issues, 2025 vs. 2024

Figure 12: Federal Funds Rate Levels Needed to Spur Hotel Investment

For the second consecutive year, New York City topped the list of most attractive markets for hotel investment due to limited supply growth, attractive relative yields and strong consumer dynamics. San Francisco was identified by respondents as an attractive market for hotel investment again in 2025 due to distressed pricing, an outlook for upside potential and attractive yields relative to other commercial real estate assets. Dallas came in third thanks to less government regulations.

More investors named Washington, D.C. and Hawaii as attractive investment markets this year than last year, while expectations for Miami cooled.

Figure 13: Most Attractive Markets for U.S. Hotel Investors

Direct market inquiries, as well as bid activity for both CBD and suburban San Francisco hotel assets, have grown significantly since Q3 2024. This has been fueled by a more moderate and pro business mandate, a settlement with the local hotel workers union and a slate of upcoming major events and conventions for the next two years. Henry Bose, SVP, CBRE Capital Markets

Who Took Part in Our Survey

The second annual CBRE U.S. Hotel Investor Intentions Survey was conducted in Q4 2024 and included over 170 hotel investors. Of this number, over 46% were developers/owners/operators.

Over half of respondents had under $1 billion of assets under management (AUM), with 52% having over 75% of their AUM in hotels.

Figure 14: Percentage of Respondents by Investor Type

Figure 15: Value of Respondents’ Global AUM (US$)

Figure 16: Percentage of Respondents’ AUM Allocated to Hotels

About CBRE Group, Inc.

CBRE Group, Inc. (NYSE:CBRE), a Fortune 500 and S&P 500 company headquartered in Dallas, is the world's largest commercial real estate services and investment firm (based on 2023 revenue). The company has more than 130,000 employees (including Turner & Townsend employees) serving clients in more than 100 countries. CBRE serves a diverse range of clients with an integrated suite of services, including facilities, transaction and project management; property management; investment management; appraisal and valuation; property leasing; strategic consulting; property sales; mortgage services and development services. Please visit our website at www.cbre.com.