Sale Prices and Brands - Historical Trends in Hotel Sale Prices

This article evaluates historical trends in hotel sale prices, ranked by brand

Introduction

Developers, lenders, investors, and public-sector clients sometimes seek advice from consultants about what brands are the best match for their hotel development goals. Which brands have maintained the highest values over time? Which brands offer the highest degree of consistency nationally? Which brands would be a good fit for a particular market? In this article, we evaluate historical transaction data in search of some evidence that may address, or partially address, these questions.

This study evaluates historical transaction volumes and sale prices within various hotel brands during the past four decades. The authors evaluated data from 11,519 hotel transactions dating back to 1970. Although the authors analyzed all of these transactions, we narrowed our research for this article to brands within the "upscale” and "upper-upscale" chain scales, as defined by Smith Travel Research. As such, the data set analyzed for this article includes 2,391 transactions that occurred between 1978 through 2009. Specifically, we included the following hotel brands in our analysis:

- Courtyard

- Crowne Plaza

- DoubleTree

- Embassy Suites

- Hilton

- Hilton Garden Inn

- Hyatt

- Marriott

- Omni

- Radisson

- Renaissance

- Residence Inn

- Sheraton

- Westin

- Wyndham

The comparative data indicates sale price trends for these brands. The historical sale price trends have been used to identify price variance. We also evaluated volatility in sale prices and transaction volume trends for these specific brands during the 31-year observation period. Sale prices, of course, can tell us something about the value of particular brands. Variance in sale prices can tell us something about the consistency of brands nationally. The historical sale prices and variance measures can both tell us something about whether particular brands could be a good fit for particular markets.

Summary of Findings

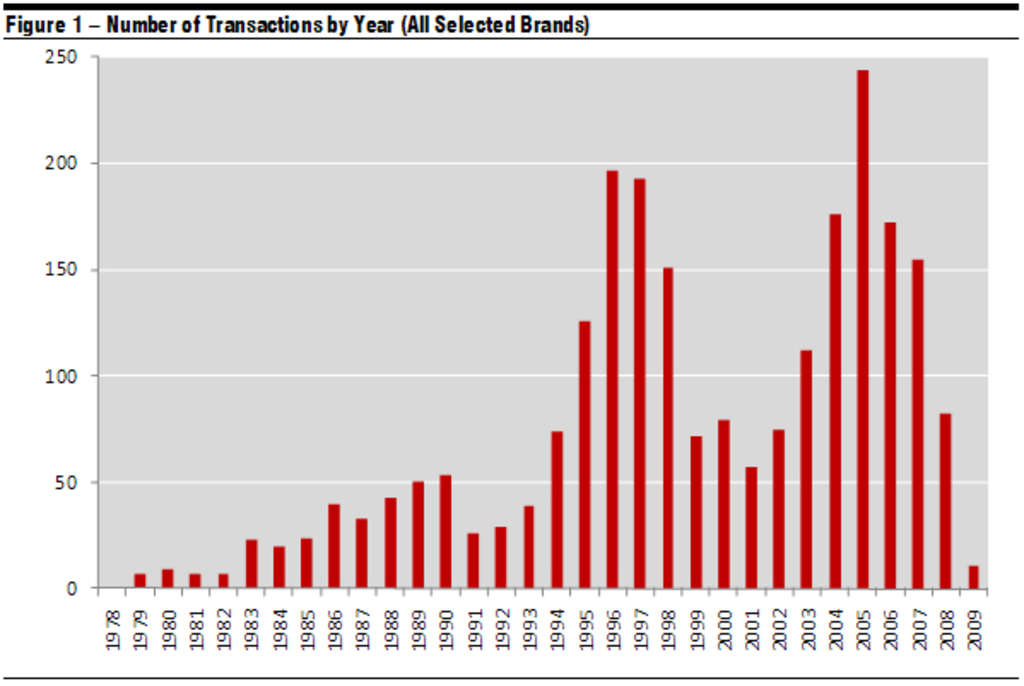

Before evaluating actual sale prices for each of the selected brands identified in this study, we wanted to review overall transaction volumes that may indicate national trends affecting all brands. By plotting the identified sales by transaction date, the authors were able to track annual transaction volumes of hotels in the data set, as shown in the following figure.

As indicated in the preceding figure, transaction volumes are volatile and cyclical within the observed brands. The volume of transactions has indicated a general upward trend during the past four decades. This is due, in part, to the trend and growth in national chains and branding during the same period. Within the observation period, however, sharp upward and downward spikes in transaction volume from year to year are evident. This reflects trends in the business cycle as well as trends in the cost and availability of capital. Within the brands observed in this study, nearly 200 transactions occurred in each of the years 1996 and 1997, corresponding with economic growth and an expansion in the availability of financing. In 2001, corresponding with a national economic recession, transaction volumes declined sharply. Transaction volume growth within these brands resumed in 2002 and peaked again in 2005 with nearly 250 transactions. In 2009, corresponding with the most recent national economic recession and tightening credit conditions, transaction volumes again declined sharply.

The average sales price per room has also fluctuated significantly from year to year, roughly corresponding with the business cycles illustrated by the historical trends in transaction volume. The following figure illustrates this volatility in sale prices for the selected hotel brands.

The preceding figure reflects a generally upward trend in nominal sale prices per room; however, sharp upward and downward spikes occur from year to year. Numerous factors may explain these sharp variations in average sale prices from year to year. For example, the location, age, and profitability of individual assets obviously affect sale prices and these individual transaction characteristics change from year to year, depending on which individual assets are bought and sold. Another factor that influences prices is the availability of financing and the cost of capital; in years when financing is abundant and capital is relatively inexpensive, there have been increases in both transaction volumes and average sale prices.

Moreover, in appraisal terminology, the "conditions of sale” can have a significant influence on sale prices. Average sale prices can drop steeply when a significant number of sales represent distressed assets with sellers under duress. For example, transactions that occurred in 2009 demonstrate a sharp drop in average price per room for Marriott and Hilton properties. However, there were only three Marriott sales and only one Hilton sale in 2009. The sale of the Hilton Montreal Aeroport represented a distressed sale of a single asset in need of substantial capital improvements, which subsequently was removed from the Hilton system. Two of the three Marriott transactions in 2009 were influenced by highly motivated sellers who may have been under financial duress. Therefore, the decreases in average sale price per room in 2009 are more indicative of the particular assets being sold and the conditions of sale for these transactions rather than some overall trend within the particular brands we observed.

For comparison purposes, we evaluated inflation-adjusted sale prices on a per-room basis for the selected brands. We converted each transaction’s sale price into 2009 dollars using a Consumer Price Index adjustment applied to all transactions that occurred prior to 2009. The preceding figure shows the average sale prices per room, in 2009 dollars, based on all transactions for each selected brand during the observation period.

The long-term price trends are much less clear when observing these inflation-adjusted sale prices. The recessionary period that ended in 1991 seems to represent one of the all-time low periods for inflation-adjusted sale prices. Another way to think about this is that 1991 may have represented one of the best buying opportunities for hotel investors during the past 35 years. The limited transaction data available during the most recent recessionary period in 2009 suggests we may be in a similar situation in 2009-2010.

The authors also evaluated the historical average sale prices for each of the 15 brands included in the study. For the purpose of this study, we compared sale prices on a per-room basis and converted each transaction’s sale price into 2009 dollars. The following figure shows the average sale prices per room, in 2009 dollars, based on all transactions for each brand during the observation period.

As illustrated in the preceding figure, the average historical sale prices range from $76,081 per room for the upscale Radisson brand to $216,732 per room for the upper-upscale Hyatt brand expressed in 2009 dollars. As expected, the brands within the upper-upscale chain scale, in general, have experienced relatively higher average sale prices per room compared to brands within the upscale chain scale.

These average sale prices within the brands represent long-term historical averages, rather than the average sale price in the most recent year. Certain brands, such as Sheraton and DoubleTree, may have experienced significant increases in average sale prices in more recent decades. Sheraton and DoubleTree are both examples of brands which were acquired by larger hotel companies during the 31-year observation period. These particular brands have a long history of transactions dating back several decades with only a respectively small portion of those transactions occurring in more recent years when the brands were benefiting from participation in the Starwood and Hilton reservation systems and loyalty programs, respectively. Therefore, the authors suggest that the average historical sale price data, shown in the preceding table, should not be used as an indication of current values for each brand. Rather, these figures represent a long-term historical average sale-price on a per-room basis for each brand.

A correlation is apparent between a brand’s average sale price and the variance in sale prices experienced within a given brand. In an effort to measure the variance around these average sale prices per room for each brand, the authors calculated one standard deviation around the mean sale price for each brand, as shown in the following figure. Minimum and maximum sale prices, within each brand, have also been provided for reference purposes.

The preceding figure indicates a relationship between the mean sale price for a brand and the standard deviation in sales prices experienced within each brand. Hyatt, for example, has a standard deviation of $126,084, which suggests a much wider range of sales prices within the brand compared to brands such as Hilton and Marriott.

Brands that experience a relatively small number of transactions can be greatly affected by a small number of sales with unusually low or high prices. To evaluate the potential influence of such outliers, the authors estimated the number of transactions occurring within each brand, as summarized in the following figure.

Brands such as Omni and Renaissance have experienced relatively few transactions during the observation period. On the other hand, brands such as Marriott and Hilton have experienced several hundred transactions in the U.S. and Canada between 1978 and 2009. As a result, the sale prices of brands such as Marriott and Hilton may exhibit a broader range, reflecting national coverage in a wider range of locations. However, a single high or low sale price (i.e. an outlier) for an atypical property within these brands will have less of an effect on the mean sale prices calculated for such brands. Note that the numbers in parenthesis represent the current total number of hotels in the U.S. and Canada for each corresponding brand.

Concluding Remarks

Long-term average sale prices vary widely from brand to brand. Numerous factors other than branding affect the average sale prices of each particular brand. For example, appraisers consider several elements such as financing terms, property rights conveyed, conditions of sale, location, market conditions, and physical characteristics as factors that influence sale prices. As such, the sale price data analyzed in this report would require numerous adjustments to provide an accurate indication of market values of the hotels within each particular brand.

The research summarized in this article also suggests that market values peak when transaction volumes peak. Real versus nominal sale price trends demonstrate very similar peaks and valleys from one year to another, but show a greater disparity in average sale prices in earlier decades. Long-term price trends are not as obvious when evaluating inflation-adjusted sale prices. Nominal sale prices indicate a trend line of relatively steep positive growth while real sale prices indicate a trend line of only slight growth. The findings in this article may be useful in evaluating branding and investment decisions for developers and may be useful in developing business strategies for certain hotel companies. However, the aggregated average figures and trends shown in this article are not intended to serve as value indications for individual hotel properties or for brands generally.

1 - Numbers in parentheses indicate the total number of hotels in the US and Canada for each corresponding brand

About HVS

HVS is the world's leading consulting and valuation services organization focused on the hotel, restaurant, shared ownership, gaming, and leisure industries. Established in 1980, the company performs more than 4,500 assignments per year for virtually every major industry participant. HVS principals are regarded as the leading professionals in their respective regions of the globe. Through a worldwide network of over 50 offices staffed by 300 experienced industry professionals, HVS provides an unparalleled range of complementary services for the hospitality industry. For further information regarding our expertise and specifics about our services, please visit www.hvs.com.