Measuring “Reservation Related Labor” for Revenue Channels

In my previously authored article, entitled "Hotel: Revenue versus Sales", I explored the benefits of using two separate but exclusive interconnected reporting platforms to analyze Gross Reservation Revenues; (1) Market Segmentation and (2) a Key Performance Indicator driven Revenue Chart of Channels. As I pointed out in that article; "A "one brand fits all" philosophy (attempting to adapt the traditional Marketing Segmentation format) may not be achievable when such varied and distinct goals regarding "EXECUTIVE NEED" are sought by each different department.

These interlinked side-by-side reporting systems, could be used to align all hotel executive needs in (1) interpreting guest need, purpose and/or the characteristics that drive their purchase decisions and (2) interpreting hotel needs in reaching revenue optimization (using demand drivers aka Key Performance Indicators).

Each Channel Ledger in the Revenue Chart of Channels, aside from being Key Performance Indicator (hereafter "KPI") driven, would show revenue and related sales executive and front desk labor costs (hereafter described as "Reservation Related Labor") and promotion costs.

Today I would like to discuss the "Reservation Related Labor" allocation.

The calculation of channel-by-channel labor is time consuming and usually performed in Accounting Departments

First allow me to point out why it is so difficult to come by complete channel-by-channel cost.

Standard hotel financial statement, using the Uniform System of Accounts

as a guide, while formidable in their own right, are not conducive to the reservation analysis process in bringing all "Reservation Related Labor, benefits and promotional costs together.

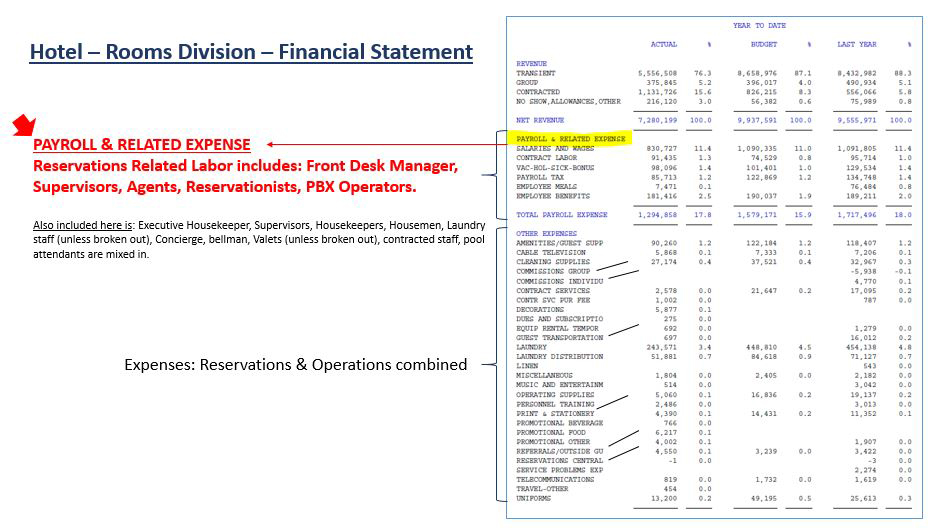

Each hotel division, and related financial statement, has a labor and benefit section. For our purposes, there are two primary divisions from which "Reservation Related Labor" is extracted and they are (1) the Rooms Division and (2) the Sales & Marketing Division. The Rooms Division combines "Reservation Related Labor" and "Operational Labor" in the same statement (See Exhibit "A" & "C" below).

The red arrow indicator above, highlights "Reservation Related Staff" that are contained in the captioned "PAYROLL & RELATED EXPENSES" portion of the Rooms Division. These include the front desk director, managers, supervisors, agents, PBX operators and Reservationists. Other positions that could also be included are the social media manager and the agent responsible for checking and/or blocking incoming reservation room nights.

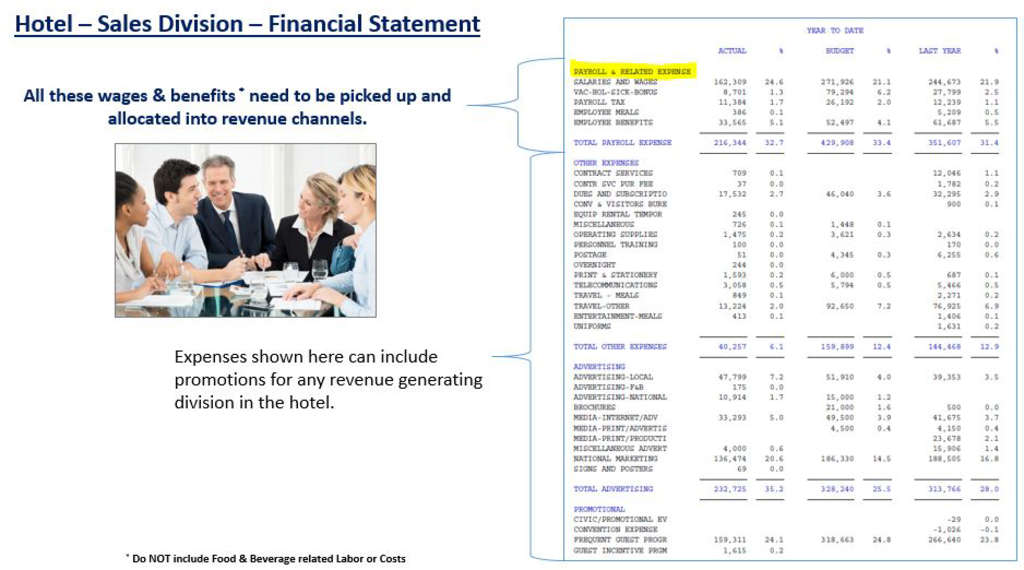

The sales and marketing related positions included in "Reservation Related Labor" are shown in the Sales & Marketing Division statement (see Exhibit "C", below).

The first question that may be asked is why include front desk wages and benefits in channel-by-channel reservation cost?

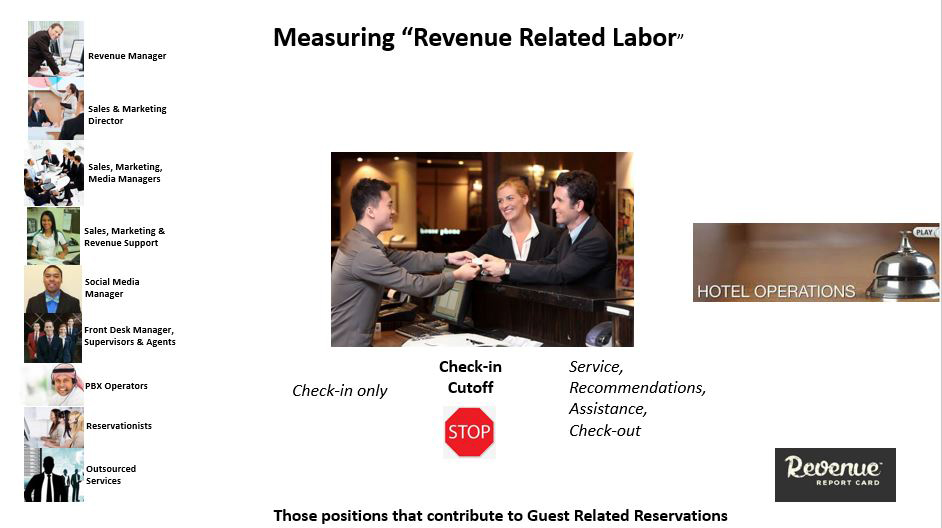

We believe that each and every expenditure incurred by the hotel toward sales, marketing, revenue management, internet, advertising and/or promotion, up until and including a portion of check-in labor should be part of the cost equation.

"Front desk agent check-in time/labor" is recognized as a variable cost that fluctuates. It's dictated by the reservation-providers

paperwork and credential requirements. Once the reservation request is received, it of course then needs to be booked into the Property Management System and in each case dictates a different time interval required to accomplish. The correct result as we see it should be that only the portion of "front desk" time/labor, directly related to "the check in process", would be included and allocated as "Reservation Related Labor". In turn, time at the desk devoted to check out, guest service, area recommendations, and/or assistance would be recognized as an "Operational Expense" and NOT "Reservation Related Labor". (See the Info-graphic in Exhibit "B" below).

In an in-depth survey of front desk managers and reservationists we have been able to determine "typical time periods" on (a) each process undertaken by (b) each position engaged for (c) each different channel from whom a reservation is received. To reiterate, each channel has a unique set of booking factors based on the different challenges presented in the booking and check-in process.

Reservation-providers

Certain reservation-providers have direct access to unsold inventories in the Property Management System, while others email or fax reservations to the hotel, and still others will call-in to make reservations by telephone. We've even recently seen on-line exclusive chat lines from which reservations can be made and confirmed. The result is that reservations continue to be both manually and directly booked into the property management system.

Blocking Incoming Reservations

We still find the majority of hotels blocking their arrivals manually, although quite a few have acquired an automated blocking module. Despite this, arrivals automatically blocked still need to be checked and depending on which method the hotel uses, will determine the time interval and labor cost that needs to be made.

Social Media, PBX Operators, Concierges and Sales Assistant Involvement

Some channels typically have guests that will engage the hotels social media, while others will call the PBX operator, concierge or email the hotel with (pre-booking) questions.

For a complete and accurate evaluation of channel-by-channel cost, this labor should be factored into appropriate channels.

It is imperative to remember that channel-by-channel costs are collected and compiled in order to determine which channels are the most lucrative to use at any given point in time. Because front desk time intervals are directly determined by each reservation-sources reservation process, different labor costs will be associated to different channels (guests).

A good example of this might be seen in analyzing reservations for Airline Crew. They can take, in some instances, three times as long as an average reservation would take to check-in because of per diems that the hotel agrees to pay to pilots and stewardesses. This is a substantial deviation from ordinary time intervals devoted to the check-in process and needs to be factored into channel cost. Upon the annual review of an airline contract and consideration of perhaps displacing all or a portion of this business, the complete channel cost must include this deviation in order to fully evaluate and compare airline business to the alternative being considered.

Displacement Analysis

With complete and actual channel-by-channel cost now calculated, a hotel has a new powerful tool in preparing displacement analysis

studies by using "reservation-source profitability" instead of the traditional method of comparing Gross Reservation Revenue to Gross Reservation Revenue! This is a decisive change in the decision making process; comparing profitability to profitability in choosing one source over the other provides a precise means in the decision making process.

How do hotels accomplish these studies?

In order to obtain precise labor and cost information, hotels need to engage there accounting departments. The allocations, are typically determined on an excel worksheet and the Controller goes through a complex series of recognizing "Reservation Related Labor" from the statements discussed and then allocating specific positions, using determined time intervals to channels . Results are an arduous and time consuming affair (the previous title located on the first page of this article entitled; "Channel-by-Channel Labor Allocation is a time consuming calculation usually performed by the Accounting Department) had started the discussion.

Currently no written standard or opinion

Besides the time intervals

involved, a second impediment in calculating complete channel "Reservation Related Labor" cost is that, there is no written standard or opinion published in the industry. One of my objectives in publishing this article is to begin a conversation in establishing such guidelines. I have presented the Revenue Report Card TM theory here today, and what we use in our program to determine channel-by-channel labor cost allocation. The program takes seconds to provide the full analysis described, but calculation can be performed in house by the accounting department as has been noted. Needless to say our conclusions are opened to interpretation and discussion. Our home page provides an expanded discussion of labor and expenditure cost and you are welcome to view it under the "Pillars of Revenue Report Card TM" section of that page at http://bit.ly/1SHKRiR ).

Hotel Financial Statements

Hotel financial statements allocate wages to many different divisions in the hotel; depending on the size of your property, there can be few or many divisions. Likewise, benefits to employees are typically compiled on a separate statement and allocated to each department according to the volume of wages in each. For simplicities sake today, I will not include the benefits statement in this discussion; nevertheless results are shown on each statement for each division.

Executives and staff that Contribute to the "Reservations Related Labor" include…

In the "Rooms Division" -Front Desk Director, Front Desk Manager(s), Front Desk Supervisor(s), Front Desk Agents, PBX Operators, Reservationists, Staff responsible to Block Rooms, Revenue Director, Revenue Manager, Support to Revenue Manager (See Exhibit "A", above).

In the "Sales & Marketing Division" - Director of Sales, Sales Managers, Marketing Director, Marketing Manager, Public Relations Manager, Support Staff, Social Media Director, Outsourced Sales and Marketing, Outsourced Public Relations. (See Exhibit "C", below).

Labor incurred DURING and AFTER check-in are Operational in nature. As previously indicated, any front desk referrals, recommendations, assistance and/or time devoted to the check-out process should not be included in the 'Reservation Related Labor" allocation. Valet, bellman and concierge service as well as room service, housekeeping and pool, beach or food & beverage services are "Operational".

Operational Services are overseen by a different "Master"

The key here is that "Operations" are administered by a different "master" and therefore we believe, need to be measured separately. This is one of the draw backs of using the well-known analytical ratio called GOPPAR. GOPPAR combines "Reservations" and "Operations" processes in analysis. While it is a good overall barometer, as mentioned it combines the work of two or more "masters". The revenue channel profitability

calculation provides the hotel with the measurement of bringing business to the hotel separately.

The following graphic illustrates the positions that typically serve the guest in an "Operational" capacity and are NOT included in the "Reservation Related Labor" calculation.

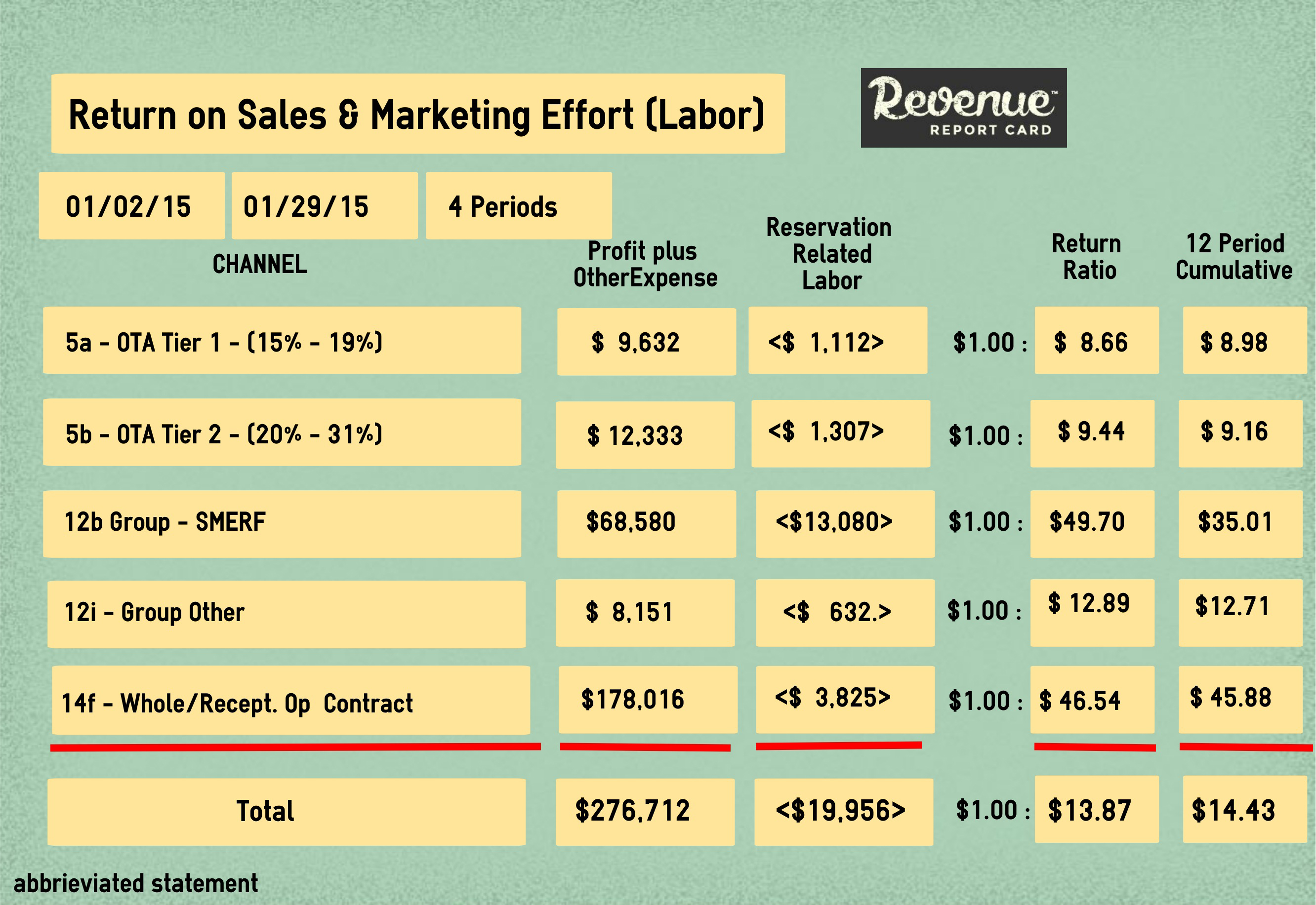

Finally, when fully-diluted labor is distributed to channels it is then associated to specific revenue streams, for which efforts have been undertaken. Simply stated, it allows the hotel executive to look at "Reservation Related Labor" as in investment, just as in any investment. An example would be amounts committed to the Automobile Association of Americas travel book. A Return on that "investment" should also be viewed. Expenditure "investments will be the subject of my next article. You can calculate a Return on Effort (Labor) in each channel. The strength of this calculation comes in several areas. First, it shows the sales teams' current productivity in all areas and those can be compared to the same periods historically. Second it can be compared to a hotels competitive set production. Below, please view Exhibit "E".

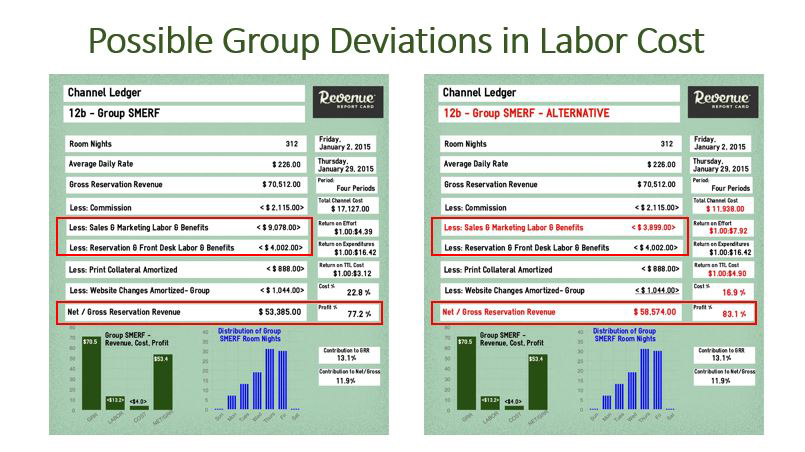

In closing, complete "Reservation Related Labor" is a critical component included in channel-by-channel cost. In some channels, such as internally generated Group and Corporate business, labor is the primary cost component of the channel. Below in Exhibit "F", sales managers, marketing managers and their support staff, along with printed collateral and internet promotion compose all costs incurred in order to bring business to the hotel in this period. You can see the difference in the Sales & Marketing Effort (labor) in these two statements. The difference in results can that (1) the hotel is carrying excessive staff, (2) the hotel is training new staff or (3) that perhaps a sales manager(s) are not performing efficiently and/or effectively. Once results are received, the Director of Sales will be alerted and a determination made on whether further exploration is necessary.

As hotels continue to make huge strides in increasing Gross Reservations Revenue by taking advantage of critical "big data" output, it enables revenue managers to make earlier decisions in confidently determining future sellout dates. Using the time before projected sellouts to their advantage, strategies can determine when high cost channels can be restricted or closed out and, in turn, fill the hotel with the most lucrative channel mix available. "Reservation Related Labor" is a key component in the study of channel-by-channel profitability.

Establishing industry standards for realizing labor allocation puts everyone on the same playing field and allows area or competitive comparisons. By evaluating performance on a weekly basis any "fall off" in productivity can be quickly recognized and addressed. It is my hope that this narrative creates a basis for good intellectual discussion. Thank you for all the comments and "thumbs up" received in my related articles previously written. They make these narratives worthwhile. Richard

Richard B Evans

President of Revenue Report Card LLC

(954) 290 - 3567