Looking Past This Crisis - The FutureState of Travel

It is quite difficult to see past the crisis of now, in any situation. But right now, in travel, it is almost impossible. Fear has gripped the world and our industry is on the front line of the response as well as bearing the brunt of the economic downturn. Airlines are hemorrhaging cash, hotels are sitting virtually empty and travelers are staying home. The crisis of right now is real for workers, owners and investors tied to the travel category, and if you want to read about how people are responding today, there is no shortage of advice, prognostications and opinions for the moment. You can even watch Bill Gates, basically, predict coronavirus in 2015.

The hopeful among us, however, will recognize that this will be over relatively soon, and albeit difficult to see, perspective and future planning is now what is necessary. Clearly recovery will be predicated on infection rates and how government intervention takes shape, and we have posted here about the possible scenarios that could play out over the next weeks and months. MMGY Global's base case for recovery is entirely focused on consumer mentality (something we are measuring weekly), in what we believe will be the four phases of societal mindset.

As we all move through these phases, it will allow us permission to spend, travel and commune again. Today we are still in the fear phase, which remains to play out as we near infection spikes globally, but understanding and action phases are now in nascent stages and rational behavior will follow soon after that. So now let's look at longer-term conditions and how we should be thinking about the marketplace in its future state.

FutureState Item #1 - Travel sentiment, activity and spending will return more quickly than many have predicted

We are seeing some consumer research, that takes an alternative POV to our own, suggesting that travelers will not return to travel in the way they have in past recessions, using current barometers that cite consumers' plans to save their money or re-allocate to other purchases versus travel. Here is an example.

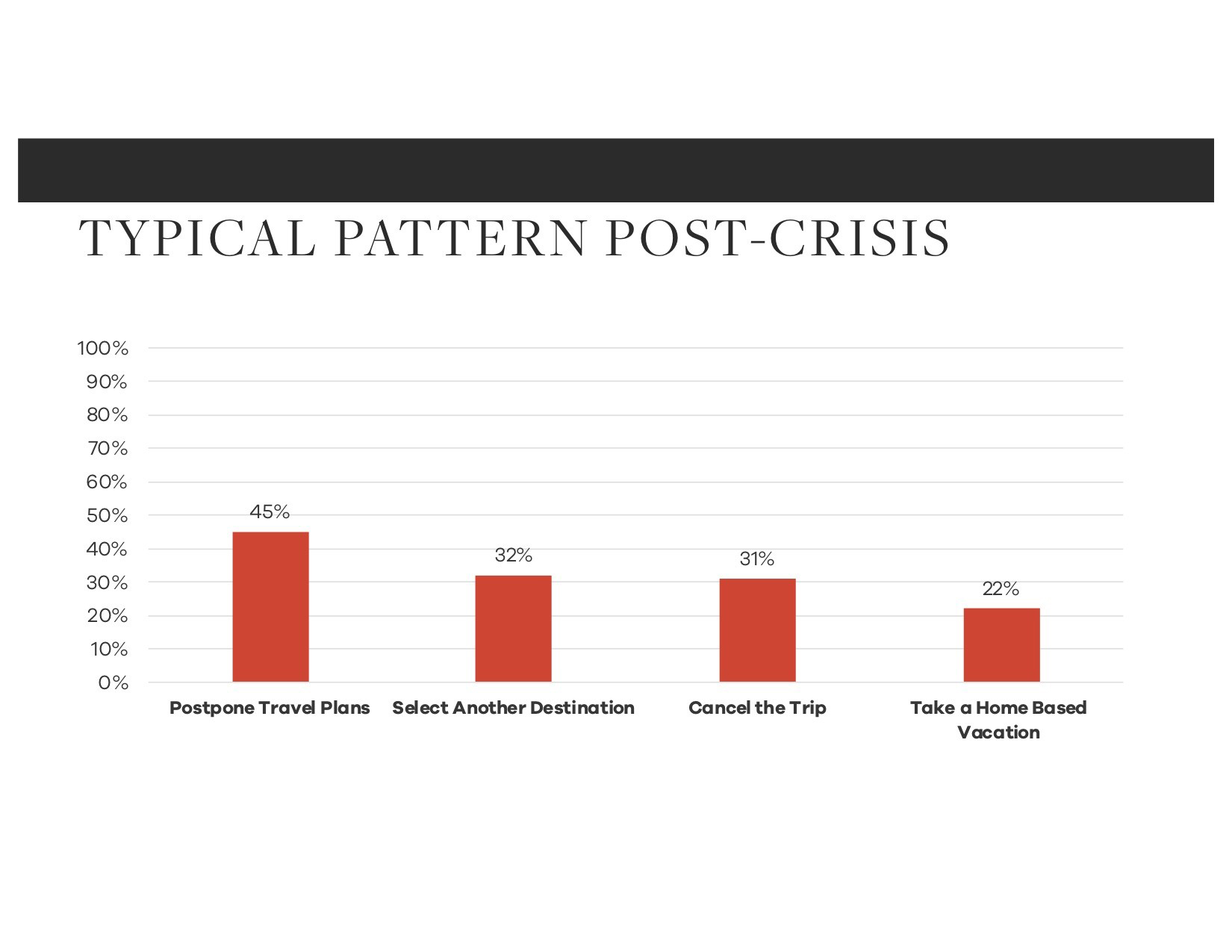

I simply don't agree, and while not questioning the veracity of this research, I instead question the real commitment of the consumer to these views. Time and time again, in the MMGY TravelIntelligence Traveler Sentiment Index (TSI), we see a much more positive mentality once a crisis passes. Instead of measuring current intent that suggests households will save the money (43%) or spend on other needs (25%), we expect the final picture to look more like this:

Here, only 31% cancel their plans, and instead they more broadly exhibit behavior that answers that global calling to travel, albeit in different ways. And even with cancellations happening en masse currently, we expect to see re-booking rates quite high amongst all consumers as the days pass. We have been tracking a "resilient traveler" segment that represents 16% of travelers, a group that tends to be most impervious to challenging conditions. These travelers will be early influencers on a return to the marketplace and are important for suppliers to influence quickly. To monitor the progression of consumer views, we stood-up a bi-weekly sentiment study, with US Travel Association - access to the results here (will be available on April 1).

Over 85% of companies in the U.S. (90% in Europe) have now suspended business travel, and Meeting News suggests that 90% of groups have canceled plans in April and May. However, a poll from Skift suggests that 33% of meetings have already been re-booked and GBTA suggests 40% of companies expect to return to normal business travel within 90 days. We know from past studies that these numbers will grow as the mindset shifts into action and rational behavior.

In Asia, and according to the ADARA anonymized data, flights in China were up 20% the week of March 8 and travel search volume has nearly doubled since February, with incredibly short booking windows. This is a reliable harbinger for Europe and the Americas, although China's virus lockdown was much more pronounced than anywhere else in the world.

Insight - Don't wait to engage travelers, they're coming back to you quickly and will book with short lead times and lower rate expectations.

FutureState Item #2 - Consumer behavior will shift in the short-term but not in a lasting way

It has been interesting to watch flash trends emerge around telemedicine, home meal delivery, online workouts and new (or no) personal grooming priorities. And those shifts certainly make sense in the short-term. But just as with past promises of virtual reality vacations replacing the real thing or Second Life becoming a surrogate for meetings, we do not believe many short-term trends will remain as structural. And those suggesting that tools such as webinars are suddenly going to replace real in-person interactions, undervalue the fatigue that is already growing with virtual platforms. We fully expect face-to-face meetings, visiting new places, cruising, socializing in restaurants, and yes even getting back to better personal hygiene, will be the norm before Q4. In fact, we have seen a long-term trend that proves out that travelers of all stripes are increasingly seeking out new and unique experiences, an appetite that will not be reversed.

There has also been much made of consumer content consumption shifts, including the massive growth rates in Netflix and live event streaming as well as online gaming. And news coverage (as well as time spent at home) has led to 11% ratings increases for network television and 29% upticks for radio listening. And of course social engagement is up substantially, while out-of-home impressions are down meaningfully as are online searches for retail and travel services disassociated with the crisis. Is any of this really surprising? Except for those still advertising in this environment, these are not meaningful data points for longer term decision making.

As part of a recovery picture, expect content consumption to be interest-based, not news-based and plan to see a return to typical retail and travel-related content - in China, travel search is up 230% since March 21st with online retail activity moving back closer to historical norms.

One change in consumer behavior we could see as longer lasting is a move back to travel aggregators and OTAs. In a competitive market, where demand is off significantly, the OTAs have a considerable advantage in share of marketing wallet and in rate visibility. Not only should CTrip, Expedia and Booking benefit, but expect TripAdvisor, Fliggy, Skyscanner and Airbnb to gain share. As it relates to short-term rentals, we might see an initial consumer pushback against staying in someone else's home space, but Airbnb, Homeaway and VRBO have aggregated inventories that will place them in a position to book more business. And then there is Google. In case you haven't been paying attention, they win no matter what. Paid search, mapping and review/content hubs as well as integrated travel booking information will still start and stop on Google. One alternative and interesting point-of-view comes from my colleague, Peter Yesawich, who suggests that suppliers will actually be in a better position because they can control loyalty-based recovery offers that are exclusive of 3rd parties.

Insight - Consumers traditionally evolve their core behaviors slowly, and even a crisis, while creating atypical "flash" reactions, don't dramatically shift trends. Stay the course with proven strategies once the crisis ends.

FutureState Item #3 - Marketing tactics will....well, basically, fall back into place

Don't be fooled by the short-term shifts in content and media consumption. Yes, the world is behaving in new and unusual ways, and there have been some major advertisers who have pivoted quickly to media channels that have been prevalent during the crisis. Informational campaigns tied to news content (ie Ford Motor Company) and in-program sponsorships have allowed relevant brands to be closer to consumers looking for crisis-related solutions. At MMGY Global, we are adopting Wait, Ready, Set, Go as our mantra for approach to marketing. This does include some current mandates to engage on PR and social channels as well as case-by-case marketing investments, but also using restraint to hold budgets for when the time is right to drive revenue into a recovery.

In the search space for example, ad spend is down significantly, with organic rankings moving up page and top paid positions non-existent for some queries. This means CPCs are greatly reduced and an opportunity exists to selectively promote brand at a much lower cost. Our client search marketing performance over the last 20 days shows traffic for travel sites down 47%, but Ecommerce CVR is down only 3.7%, suggesting that people are still booking, although on much smaller volumes. This demands that, although travel is nearly non-existent for the moment, travel brands should not be pausing paid search campaigns completely. Take a look at one hotel's room bookings in out months tied to search.

Looking forward to a recovery model, there will be some nuanced marketing changes necessary to capture traffic in the first 30-45 days, prior to widespread travel demand:

- A conservative advertising presence to capture the "resilient traveler" subset as well as other early adopter consumers. A focus on performance-based digital that is value-driven and informational as well as steadying for the traveler

- Social engagement to both educate and keep close the most valuable customers

- Campaigns that encourage near-term travel such as weekend, last minute and holiday packages as well as short-lead Summer travel packages that incorporate loosening cancelation and re-booking fees

- Geo-targeted campaigns that work community-out for stimulating demand

- For DMOs, pushing some advertising investments and coop programs into local consumer markets, with content to establish local trust that pays dividends with out-of-town guests as well

- In the group and FIT segments, focusing on sales programs that are informational in nature and that provide visibility on revised rate packages and contract conditions while also responding to the current influx of force majeure conflicts

But travel marketers should expect time-proven tactics to be important as the recovery mindset shifts (45-90 days after peak infections) to normal behavior, and the reality is that this is where markets will be re-shaped by smart brands who remain present. For example:

- expect PPC & meta, paid social, addressable media and email programs to again be the most effective channels for down funnel, value-focused messaging

- expect linear & digital TV, PR, out-of-home and integrated print to be relevant in building brand

- expect brand partnerships, integrated sponsorships, live events and endemic content to rise in importance in building traveler trust

- look for website platforms to evolve away from deep stack encyclopedia-based models to content hubs that tie to personalization and improved usability based on user-data

- expect an emphasizing of relationships with intermediaries such as Helms-Briscoe and consortia such as American Express as well as a hypersensitivity to how tour operators and wholesalers are building back support

- more work with travel trade and travel media to collaborate on offers and content as well as aggressive sales tactics from NSOs and in-house sales teams

- expect 3rd parties to become more valuable in inventory merchandising, especially content tied to OTAs, tour operators and other aggregators

- For 2020, and perhaps 2021, expect corporate travel policies to be tightened and for in-house travel departments to have increased influence on FIT

Insight - Most reaction to today's marketplace should be minimal as it will be too late to capitalize once implemented - better to build 2020 Q3/4 and 2021 strategies that respond to the post-crisis mindset and were germane prior. Don't overthink it.

FutureState Item #4 - The industry will come back in a way that's predictable

Our research, and increasingly economists around the world, are now suggesting pent-up demand will be unleashed in late Q2 across global economies. Given the $2 Trillion+ Congressional package in America and stimulus programs throughout Europe, suppliers will be in a more tenable situation to operate with less disruption. And we know that travel confidence leads-out consumer confidence, therefore will be a leading indicator for the economy. Expect shoots of good news to emerge first with airlines then hotels, restaurants and cruise lines.

So how does the market recover, in terms of traveler type and segment? Where will the first signs of life emerge and how should budgets be allocated to different opportunities still this year. We know that leisure re-starts first, followed by corporate and group, so let's start with traveler trip-type:

As has always been the case in a leisure recovery, it starts with the local community and works itself out over time to longer-haul travel. There are certainly micro segments that will behave in more specific ways (Older retirees & Millennial families on road trips or high-earning couples to international destinations), but broadly people tip back in with shorter, closer trips and lower spends. Suppliers and destinations that rely heavily on an international traveler will still need to immediately ramp-up marketing and representation models to ensure protection of marketshare, but it may take longer to realize total revenue recovery.

We have past data that suggests corporate and group travel to be a laggard to leisure (by one quarter), meaning Fall, 2020. Traditionally certain segments of commercial business, as noted here, perform better in the early stages, with high-spend corporate and city-wide conventions slightly in the rear to SMERF, Unmanaged commercial, FIT and Association. Availability for re-booking make this a puzzle for convention centers and DMO sales teams. And prognostications that video calling and virtual meetings will reduce the need to meet is fallacy. In fact, we believe the current "home sentencing" will induce over-indexing for corporate and group travel over the mid- and long-term.

In terms of specific categories of travel, there will be a bifurcated transportation that will drive the resurgent demand; the airline recovery and travel by car. Road trips have been on the rise for five straight years, and 2020 could well become the year of the car. In our initial look at consumer sentiment, we know that traditional road trip customer segments (such as matures and families) will look for regional leisure experiences, but expect business travelers and non-traditional leisure segments to be more inclined to jump in the car, too. This is good news for the economy hotel space, smaller DMOs, attractions (and perhaps even Amtrak) but less helpful for rental car, rideshare and long-haul travel. Even in Europe where fares are relatively low and where cross-border flights are common, we would expect travel volumes to increase by car (or train).

Airlines - Given global government assistance, we expect airlines to bring capacity back quickly and use low-fare strategies to induce people to fly (vs drive or staying home). Ultra Low Cost Carriers (ULCCs) such as Frontier and Ryanair look to be well positioned while there are other small carriers that might not survive a cash crunch (read this story from Phocuswire on the financial fallout). The big global players, however, will bring routes, labor and promotion back as travelers show early demand, which is good for the rest of the industry. Look for an initial air service that could have a stripped-back experience relative to amenities and customer service.

Cruise - Many people underestimate the ability for cruise lines to survive and thrive in the new reality. Don't. 1) They have a great deal of cash (CCL and RCCL) and 2) They have a built-in sales force of international travel agents that will help grow back demand. Yes, there has been some association with Covid-19 to cruises, but as the virus proliferates to all reaches of society cruise will not be the lasting narrative.

Destinations/Attractions - Tourism and convention destinations have the most flexibility in travel. As the recovery begins, local communities will prop-up restaurants, attractions and hotels before out-of-market demand picks-up. And, local meetings and events should help in the interim period before destination groups re-book. We would expect that many cities will over-emphasize leisure marketing to offset convention shortfalls. DMOs should also be able to connect again with tour operators and airlines to develop recovery strategies along age-old traveler source markets. There will be a future funding headwind as lost bed tax and government support weakens year-over-year, but politicians should better understand how tourism is an economic lever for recovery and will find ways to supplement budgets.

Lodging - Nobody has been hurt more than the hotel industry. With global occupancies in the single digits and high fixed-expense, many independent owners will be on the brink. Remember that brands such as Marriott and Hilton are affected by lower franchise-driven fee revenue, but they own only a small number of their flags, so big owners such as Blackstone and small business operators of single units will also need support. We expect a great deal of early "local" occupancy to start the recovery, followed by leisure in the economy and luxury/resort segments and then, eventually, corporate and group across all segments. The biggest challenge for lodging is how to maintain ADR in an aggressive market grab, and in an environment where available rooms are at historic highs. Watch for campsite operators, such as KOA, and outdoor attractions (such as mountain towns) to see increased demand early in the cycle.

Rental Car/Transportation - People should be talking more about the rental car industry, and the net affect on their operations. Enterprise Holdings, for example, is one of the largest privately held companies in the world (larger than Southwest, Disney and Carnival). Outside of insurance replacement, where MMGY doesn't have a lot of information, the halt of travel has squeezed all of the global car rental operators. Most cannot draw down their fleets and therefore have enormous carrying cost. But, the industry has largely consolidated already (as with the cruise industry) and have the ability to survive, though it is likely to see smaller independent airport brands disappear. Shared ride will also see declining capacity for the balance of 2020 as both consumer sentiment and driver availability will be diminished. This will help rental car marginally, and we expect to see the large rental car brands pivot to local rental and "road trip" packages that encourage people to leave personal automobiles at home.

Insight - There is a relatively reliable cadence to the way industry and travelers will recover. Paying attention to these patterns help make marketing investments more efficient and guide investments in partner and sales programs across industry.

FutureState Item #5 - Long-term strategies still apply

It is very difficult to resist strategy shifts that rely on the data of the moment. A knee-jerk reaction can mean missing opportunities tied to core strategies that travel brands have been building for years. There are many marketing and operational examples of this, but here are just four we feel are crucial.

Strong Revenue Management - it is easy for me to say, but industry must resist a long-term, deeply discounted rate/fare strategy. We know it is necessary in the early stages of recovery, but when looking at the longer booking windows and select parts of the market, maintaining as much rate integrity as possible will beget a faster and more sustained recovery. Nobody benefits from a price war.

Sustainability and Social Responsibility - the consumer may place less emphasis on social purpose and the environment in the short-term, but we believe we have reached a global tipping point for what travelers expect from their preferred brands. And the fact that a worldwide pandemic has required a community response should portend a larger focus on social empathy.

Brands that take an integrated approach to their values, and then connect this with strategies around sustainability and social good, will continue to grow marketshare versus companies that abandon these efforts.

An Interconnected Travel Economy - will continue unabated as we move back into travel as normal. Though there will be some short-term moves away from certain aspects of freelance workers and shared services, the principals of the GIG economy will persist for the longer-term. And in fact, as people see tougher financial conditions over the next 12-24 months, don't be surprised to see new shared space concepts come to pass in personal retail products, consignment clothing, education and through a general re-balancing of societal interactions where people rely more, not less, on each other.

Use of Data is Still the Game Changer - those that continue to invest in understanding and deploying first and third party data strategies will outperform. Micro segmentation, enhanced modeling and attribution as well as the ability to connect this data to Closed User Groups (CUGs) and promotion will protect customer share and boost rate integrity.

Be optimistic

Things will get better, a notion more people need to embrace. And although I intend no disregard for the real suffering going on, thinking macro and thinking positive are a choice. There is no way for anyone to know for certain what the next 60, 90 or 120 days look like, but we know that recovery will happen, sooner than people can see clearly today. Based on progressions in other parts of the world as well as allowing past research to inform the crisis, we know that travel is a bedrock for economic stimulus. It's time to begin the move away from the fear & reaction of now, and instead begin preparing for the future state as understanding, action and rational behavior take hold.