Travel in 2021 Will Be Better And Worse Than You Think

As we all process the short and long-term effects of COVID in our lives, jobs & leisure pursuits, I have been conflicted with the reality of a very real lethal threat to the world community and the incredibly important role travel plays in the success and lifeblood of small business, service workers and government tax-based human services. Yes, we need to wear masks, socially distance and protect others, but we also need to move our economy forward with travel as a lead economic boon.

In March, I shared this POV and still believe that many of our insights hold true and remain good guidance for the future. But I also must admit that the global cost, in terms of lives and economic struggle, has been larger than I ever expected. Over one billion people have been impacted by the virus and close to $2 trillion has been lost in travel, in addition to the over 4 million jobs lost in the U.S. alone.

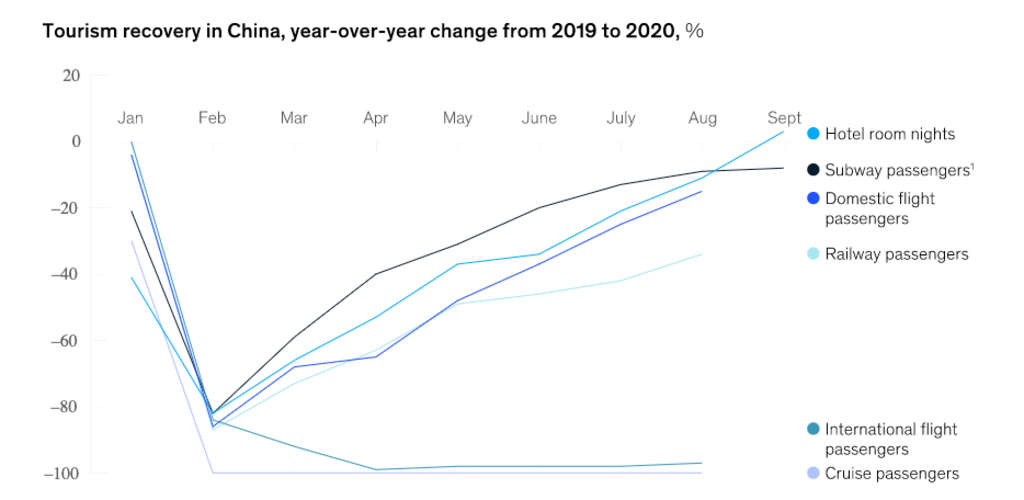

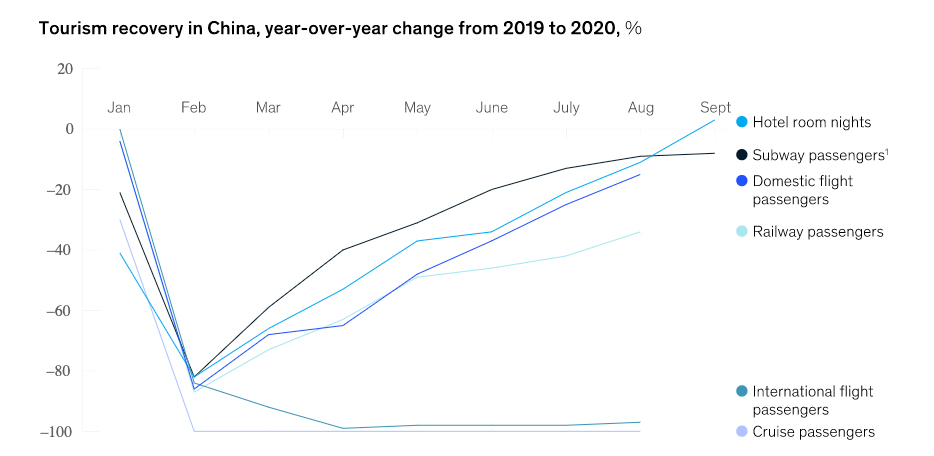

As we look into 2021, there are many reasons to be optimistic as travel intent is climbing and vaccines are on the near horizon. In China, hotel occupancy and domestic flight numbers are now 90% of 2019 levels and in a study from McKinsey, Chinese intent to travel rose from 15% to 70% between May and August.

So, what does that mean for the year ahead in terms of demand, short-term trends and long-term impacts in the rest of the world? Can we expect a quick bounce like many parts of Asia are experiencing?

The Consumer Mindset

As we talked about in March, travelers have moved through the four cycles of Fear, Understanding, Action and Rational Behavior over the last nine months. You see it in the MMGY Travel Intelligence intent data that reflect moves in and out of this cycle.

Most interesting are the quick pivots consumers made as they began to understand the virus and the precautions necessary to travel safely. Flight, occupancy and visitation numbers continue to be devastatingly below norms, but consumers have slowly tipped into travel albeit in different and constrained ways. As with the post-9/11 travel period, people will now prioritize travel in new ways that allow a connection and authentic experience that acts as a salve for the sense of deprivation in 2020, both in leisure and business settings. This socio-economic and emotional reality, in aggregate, sets-up for a very strong demand recovery despite the prognostications of some industry analysts.

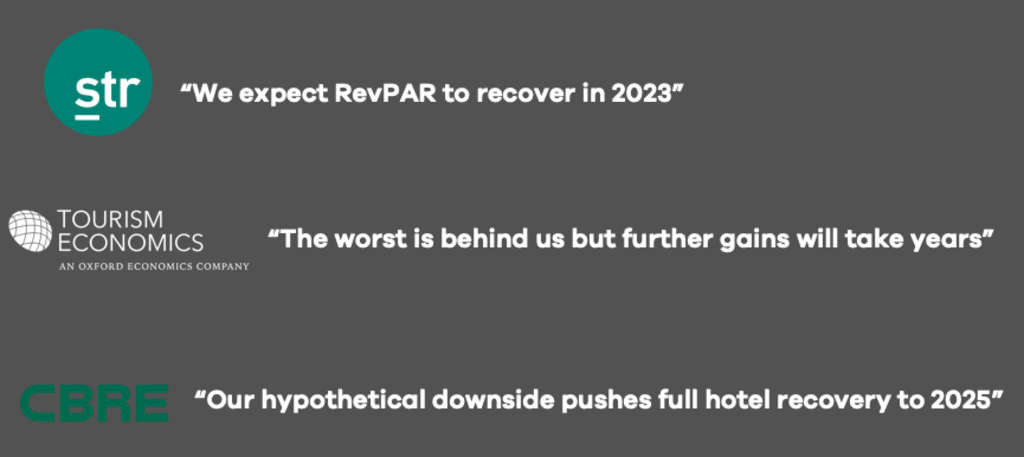

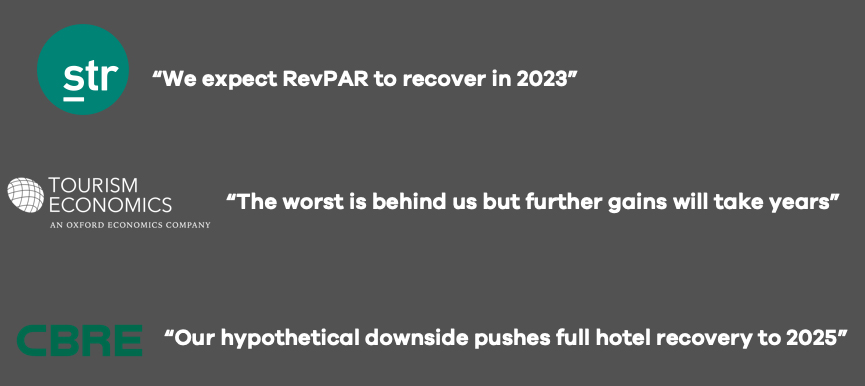

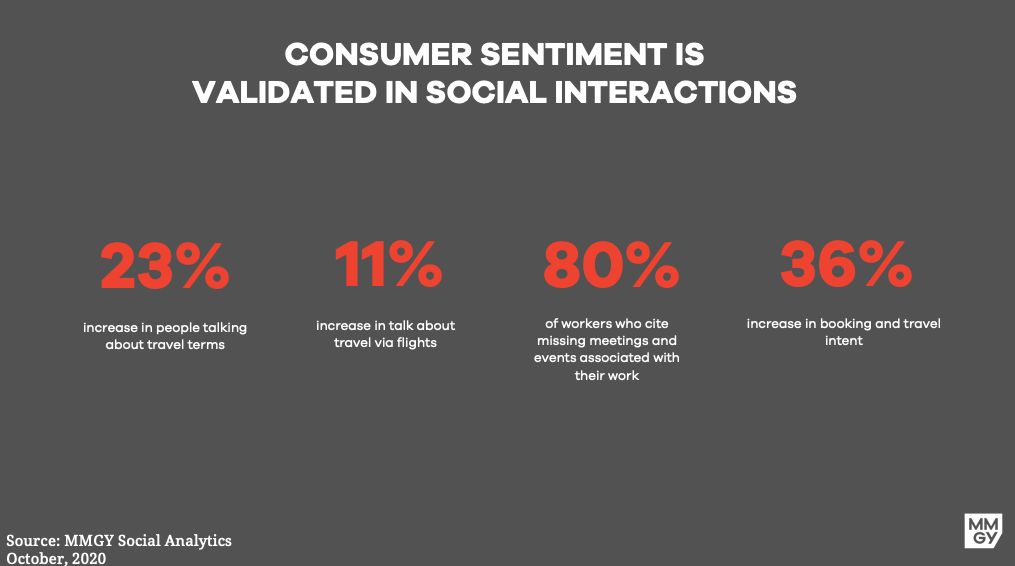

While some suggest 2021 will reach only 70% of 2019 travel revenues, we think it will be much higher with a global travel recovery reaching pre-pandemic levels by early 2022. We think this could mean growth records in Q2 and Q3, though it will likely be a "K-shaped" recovery, with winners and losers. We base our more positive forecast on how intent data historically plays out, plus a much stronger household economic standing than was in place during past "recessions." Savings rates are at peaks, consumers have been restricted in their movements (and therefore spending) and businesses have gone months without seeing customers and colleagues. As additional evidence, there is growing optimism in our social analytics tracking data that, along with the announcement of global vaccines, will lead to stronger than anticipated activity.

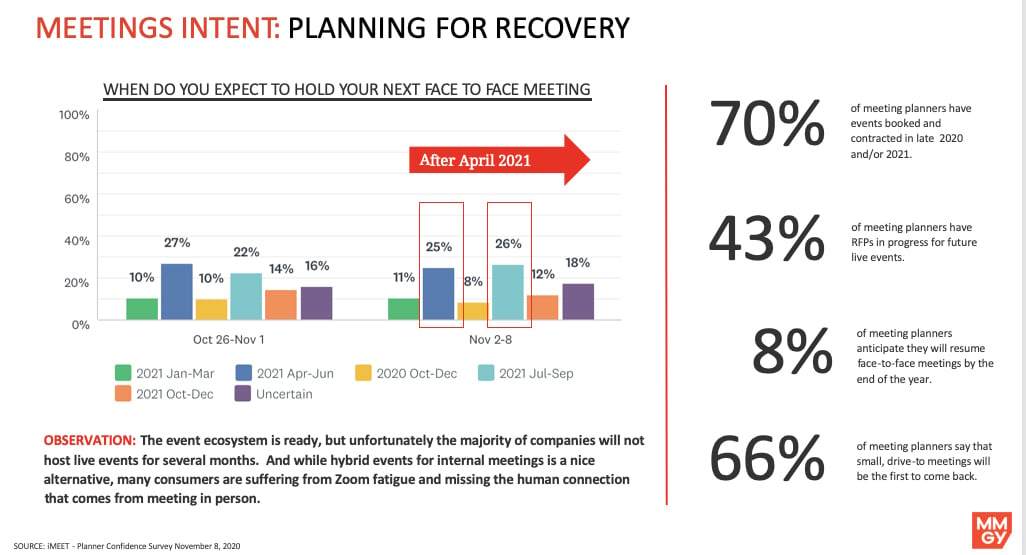

In MMGY Travel Intelligence surveys ending 2020, just over 50% of travelers told us they will get a vaccine immediately, but this data from Kaiser Family Foundation is much more hopeful for wide acceptance. We believe that 2021 will introduce a new vernacular around the rollout of vaccinations, almost a peer pressure to receive the shots. In travel this could very well take shape as a requirement to "pack your vax," if want to engage with suppliers, events and venues. We see vaccinations as a line of demarcation before many people will enthusiastically embrace collaborative work space as well as large leisure gatherings, and it is likely to become a social expectation (if not regulation) for global travelers to be vaccinated. Perhaps we will see vaccination vacation packages in 2021 or a trend tied to a term we have coined, "Vaxication," to commemorate the first trip people take after treatment. In this way, the timing of vaccines is quite important to a recovery timeline.

The lack of travel this year has created a window of opportunity for start-up concepts such as Under Canvas, Selina, Avail and Bunkhouse, as we often see disruptors born in challenging market conditions. As travelers signal in our research that they desire something more original and authentic, new brands and travel experiences will have an opportunity to create a market.

The Business Mindset

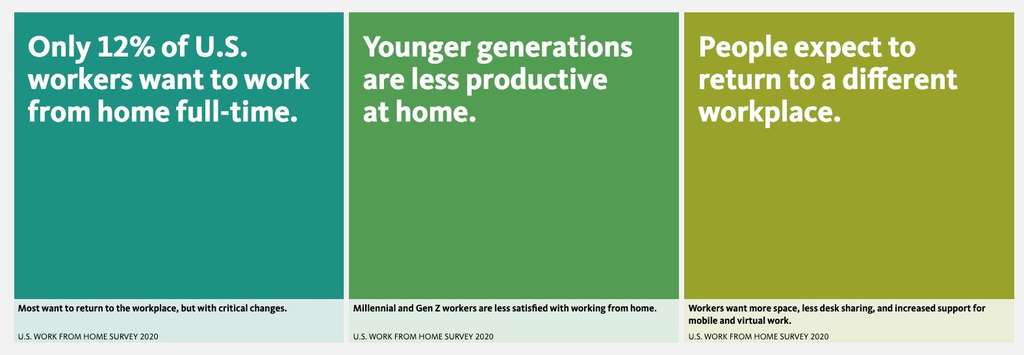

Corporate FIT, most group business as well as commercial event volumes are basically non-existent today. To this end, many are calling for a 2021 continuation of low business travel investment in favor of virtual meetings and a new world order that keeps people in their homes and off the road. We just don't believe this. Recent articles from the LA Times, Washington Post and others point to planned reinvestment in the commercial core and what will be a concerted effort to bring businesses back together into physical space.

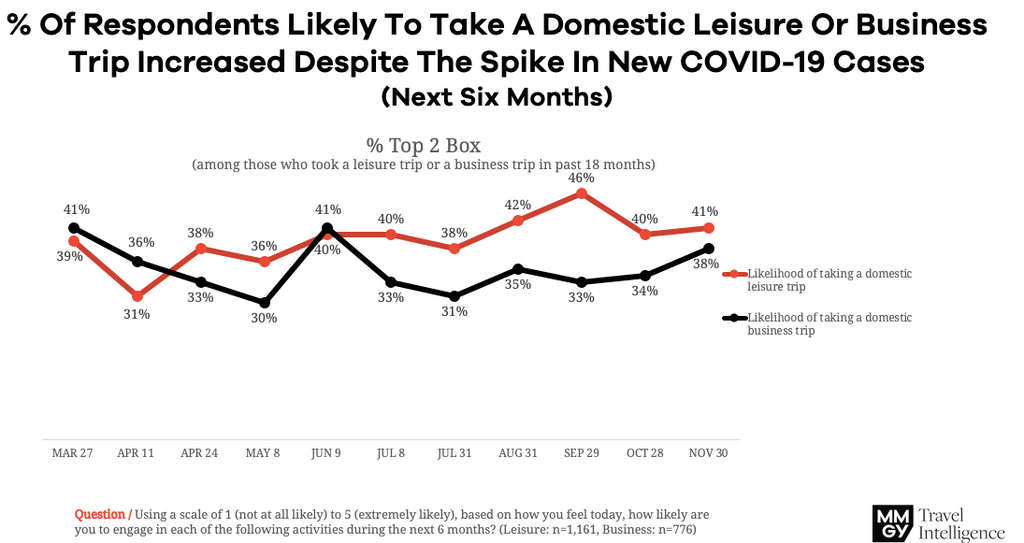

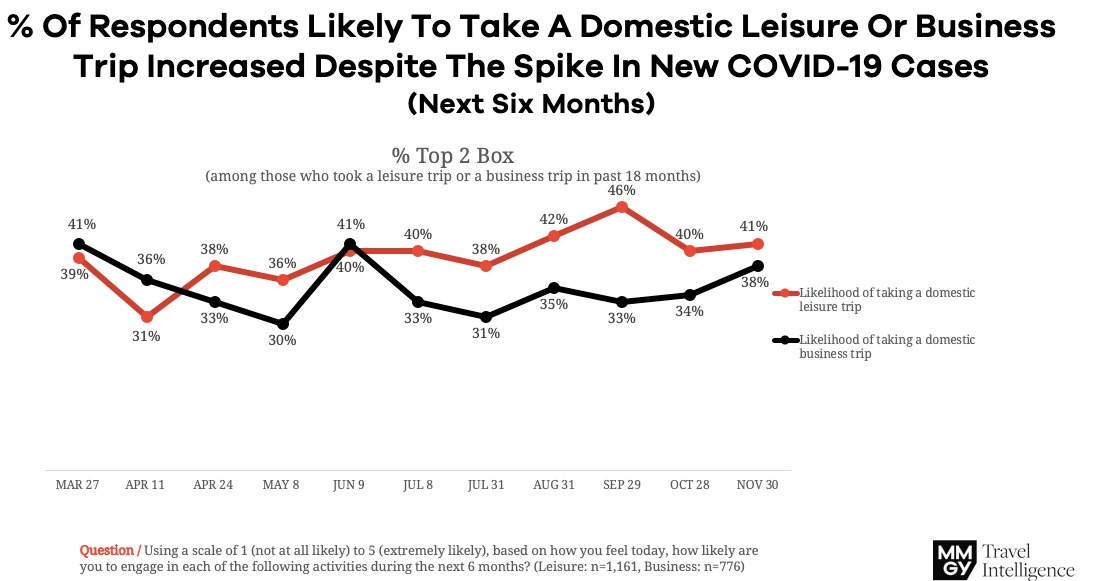

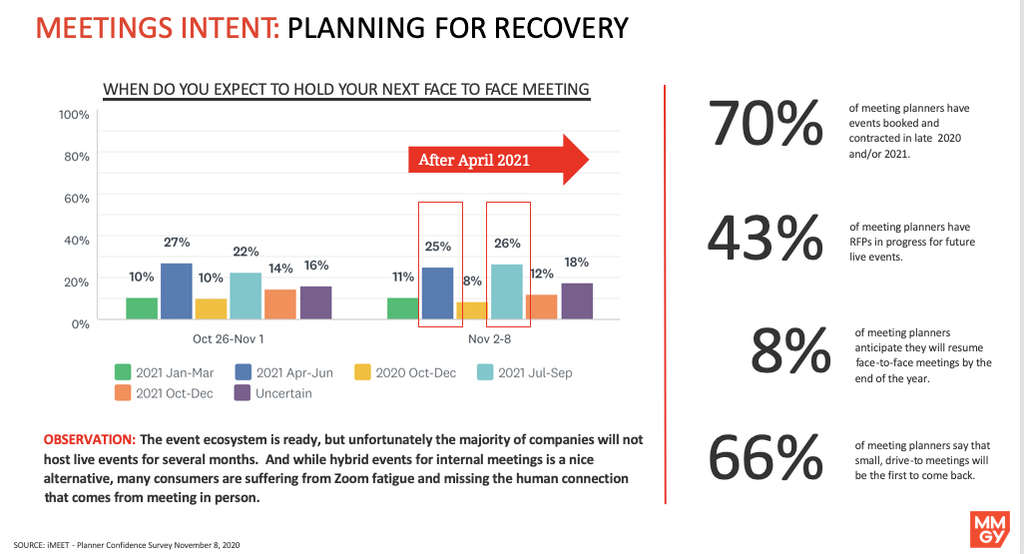

Not only do most CEOs and staff want to be back in offices and working in collaboration with clients and colleagues, but business travelers themselves are beginning to signal a pronounced need to travel. Both corporate travel and meeting planners are becoming more bullish as the vaccinations have been announced (20% remain concerned with company liability without it), and in our most recent December survey, 57% of business travelers intend to take a trip in the next six months.

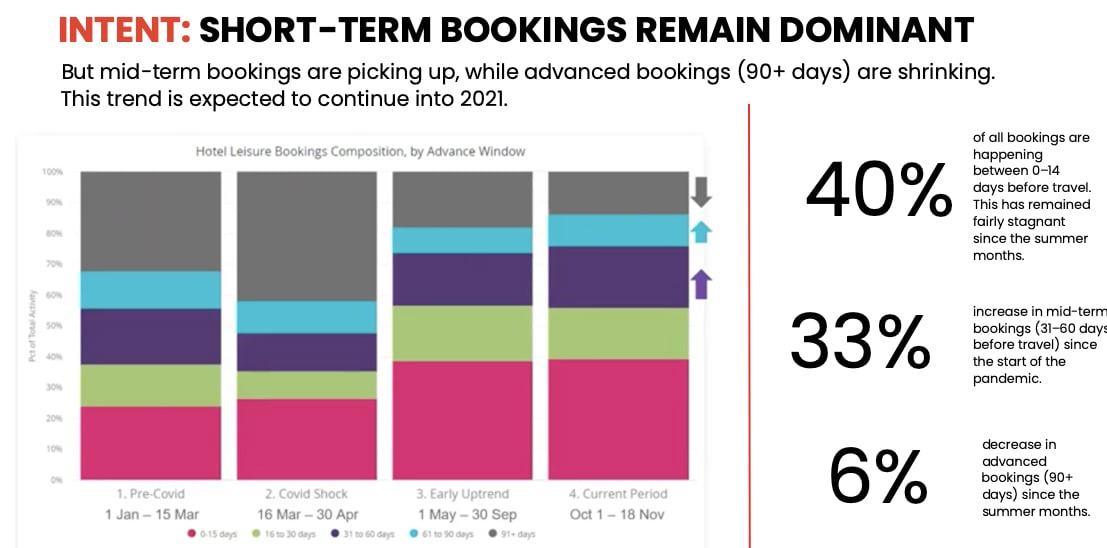

So both leisure and business travelers are becoming more hopeful. We also know that many who say today they will not travel, will change their minds relatively quickly after the crisis narrative shifts, so short booking windows mask demand that cannot be seen in longer term forecasts. We have seen similar dynamics coming out of Zika virus, terrorism events and other market disruptions. Booking windows will stretch again, once conditions normalize, but revenue management strategies will have to adapt in 2021 based on a much more fluid shop-to-book funnel.

Industry vertical snapshots

Airlines: Expect another round of stimulus for US carriers ($15-20 billion) as revenue declines have worsened. We should anticipate that airplanes will be kept on the ground into Q1 2021 to help strengthen fares and keep costs reduced, with a focus on smaller route maps, non-traditional service patterns and leisure-driven operations until commercial demand returns. We also expect intent to pick-up dramatically in Q2 and international traffic will actually outperform domestic recovery, on a relative basis, once the business community sees normalcy. We believe many tertiary routes will not be restored immediately, as border and business openings return in phases, but we do expect major global carriers to seed mainstay routes in the spring. Expect Ultra Low Cost Carriers (ULCCs) to return to profitability more quickly on the pent-up desire for low-fare leisure travel, while much-needed commercial traffic will grow by June but without immediate operational profits. Long-term, the biggest carriers will emerge strongest as they consolidate code-share arrangements, lever loyalty-based service levels and take more airport slot control. They will also benefit significantly from the deep cost cutting done during the pandemic.

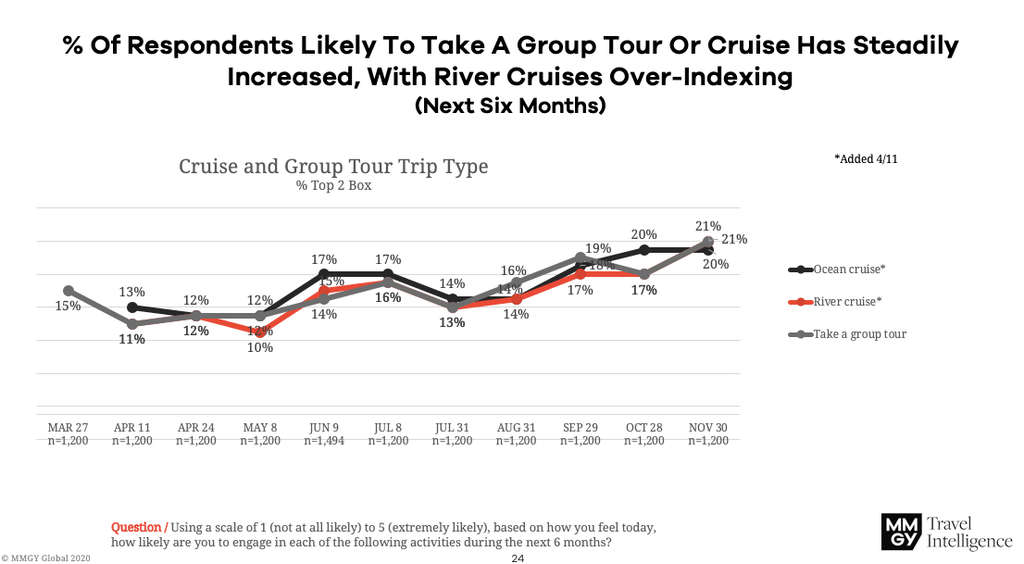

Cruise: Most of the major cruise lines and have rolled 2020 cancellations into record 2021 bookings. Though this industry has been hardest hit in terms of both revenue and perception tied to the virus, it is clear that the category's best customers are also amongst the most resilient and hopeful travelers. Though there will be some reduction in itineraries for 2021, we expect strong demand, even in the midst of an average customer age that continues to skew older. We also believe that, although travel agents have seen a substantial reduction in business, they will re-emerge quickly and provide a tailwind for cruise bookings. In the short term our data suggests US & European river cruises, newer ships and brands that embrace safety protocols will outpace others over the next 18 months. We could also see more consolidation in the category globally, with weaker lines folding into the big three (CCL, NCL and RCCL).

Destinations: Albeit down across the board, there is a significant bifurcation in the visitation numbers for cities, states and countries this year. City center hubs have borne the brunt of the travel recession, because group business is non-existent and the closing of restaurants and many attractions in urban environments has greatly diminished the visitor experience. At the same time some communities across the US and Europe have seen good demand for drive-to/train-to locations and in places that offer outdoor experiences. It has been an uneven decline. For 2021, we see three major outcomes to consider. 1) We expect commercial demand to return to major cities faster than many predict, largely tied to association, small corporate group and a sudden FIT growth around sales activity. 2) Residents in leisure-focused communities now have a more guarded attitude about visitors and this could challenge policy and tax support for some DMOs. 3) Strong tourism communities will fund recovery in creative ways, while others may see fewer resources given smaller bed and consumption tax generation in 2020. As a result, expect DMOs to move more significantly into visitor data/understanding, loyalty, partner programs and community engagement as they become aggregation points for recovery, both in terms of small business needs and visitor information. This could pave the way for new revenue streams and government support.

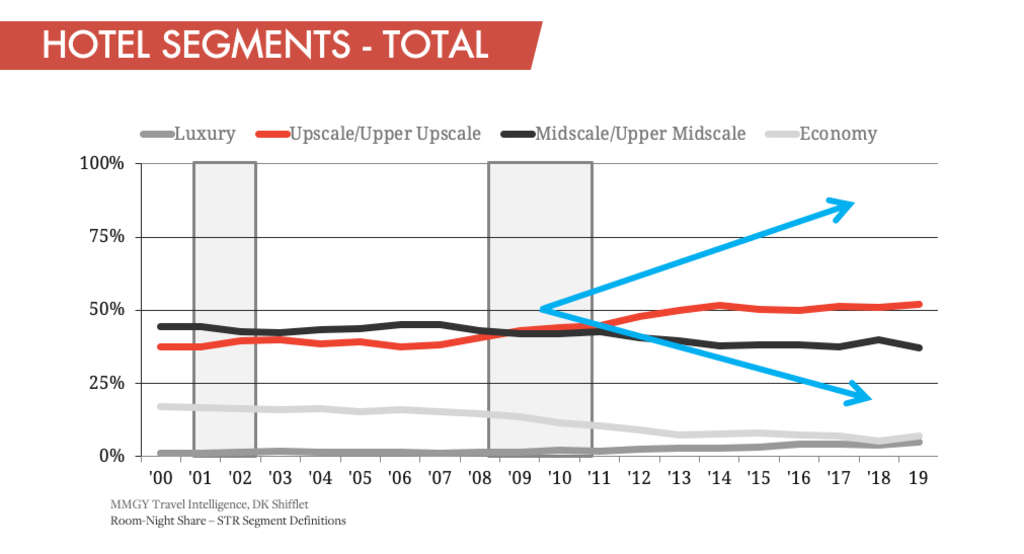

Lodging: Early recovery has already started for leisure resorts in mountain and beach locations and pockets of economy lodging exceed 50% occupancy today. Shared accommodations and rentals have also strengthened their marketshare position while city center and large group hotels still need nine months to create group compression. It is clear, though, that meeting planners and corporations have signaled stronger intent since the vaccine announcements.

We expect consumers to drive 2021-22 rate strength in seasonal leisure destinations and the high-end of the market will perform well (in a post-recession rate environment that, in a departure from norms, will keep prices strong). As it did in 2010, the economy segment should continue to over index the middle-market hotel categories as travelers trade up or down based on their situation.

Owners with assets that were already underperforming the market will likely be liquidated or be forced to re-develop, and we already see hotels re-imagining their space with ghost kitchens, local work hubs and room blocks used for charities. In a low-rate debt environment, more hotels will be built, but do not expect the truly special hotel assets to change hands or close. We do think core brands (the big six of Accor, Choice, Hilton, IHG, Marriott and Wyndham) will be more relevant in recovery, tied to central sales/technology as well as the need for an institutional "theater of clean" and broad distribution. As for newer players such as Oyo and Sonder, the recovery landscape could make it more difficult to deliver on growth plans, especially as Airbnb snaps up more rooms. And speaking of Airbnb, the re-fashioned OTA has certainly picked-up momentum as the accommodation of choice during the pandemic. The IPO was a spectacular success but regulatory and inventory issues remain fundamental challenges for their model.

Transportation: Rental car and shared ride were affected as much as any industry category in the early stages of COVID. But Uber pivoted to delivery and other parts of its business model (Lyft was less diversified) while the largest rental company in the world, EHI, levered its insurance replacement and stand-alone business model to weather the storm. Most interesting though, and despite Hertz being in the midst of bankruptcy, the second half of the year saw a stimulated demand for rental cars. AvisBudget actually netted a profit in Q3 and the largest rental operators saw a growing demand for car travel via rental. We expect this trend of recovery to be more pronounced as airports return to more normal volumes, while at the same time roadtrip rentals will remain strong. Our current data shows growing intent and because fleets were sold off late in 2020, some rate compression will be in place as well as reduced operating expense. There should be a short-term return to rent vs shared-ride as travelers continue to manage expectations around personal control and clean.

Marketing Shifts

To us, distribution of inventory and the role of intermediaries is the most interesting dynamic coming in 2021. OTAs will be more important, corporate travel policies will be more strict and the impact of loyalty programs that are currently in flux will have less influence. Despite all of this, a rate environment that will be more supplier-favored means more rate integrity than we have seen in past recessions. The explosive move up in YOY demand in 2021 should help all travel brands get back to profitability more readily, and the sales and marketing organizations that are best prepared for the rally will shift share. We also expect traditional travel advisors to be more relevant as travelers seek clarity on the travel experience. It will be interesting to see which global booking platforms evolve to better merchandise inventory for up-selling flights, accommodations and tour activities, in a race to control more spend per trip. Peek has made progress in bundling trip components but enterprise platforms are not yet there and it's time they innovated.

Liability protections and the perception of safety will be crucial in the coming months. We know from our December sentiment survey that travelers and corporate decision makers see both as table stakes, while as many as 20% of meeting planners cite liability concerns related to COVID-19 as a major barrier to booking large groups.

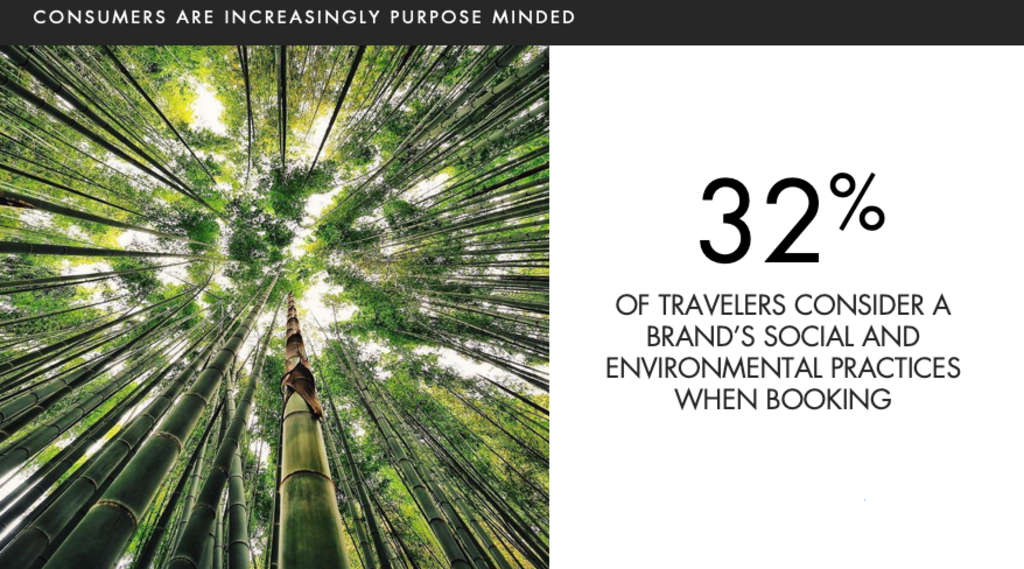

While marketers are in the beginning stages of lighting a fire of new demand, the advertising landscape itself is changing, too. Privacy controls are becoming more stringent, brand "purpose" is more important than ever and travelers have higher expectations for both product experience and value inducement.

This means a data and CRM strategy is crucial for best-of-class companies. Connecting data intelligence to micro behaviors to closed user groups (CUGs) to seamless transactions through mobile and app is fast becoming reality. It is what successful new travel platforms such as Uber, Airbnb & Hopper have done and what is required of legacy brands now, too. Those that can afford to invest in these technologies will control more direct revenue. AI-based revenue management systems from companies such as Duetto or real-time rate promotions through smarter programmatic ad networks promise a more effective digital marketplace. As Google looks to phase-out cookies in 2022, marketers will place a premium on developing permission-based engagement platforms through loyalty and partnerships.

During the time in which many of us have worked from home (WFH), or worked from vacation (WFV), we have changed the way we consume information.

Social media and entertainment content consumption are at all-time highs. Contentious political environments around the world have changed the ways in which business is done. And a transformative awakening of social justice has asked of all of us to be more inclusive and thoughtful for the underrepresented communities around us. So whether it is the effects of Brexit on business travel or the way U.S. communities better embrace diverse travelers, marketers must be aware of these social changes to ensure their brand and customer engagement strategy remains relevant.

Operational Realities

As consumers are eager to return to travel, our industry must still grapple with the challenges of a re-start. Some issues to consider:

Airlift

The global route map is much smaller today, with planes on the ground and operations staff at much lower levels. How quickly can planes and people be re-certified and which city pairs might face limited air service even as travelers intend to visit those communities? Will airports be more easily navigated or are new border and health controls poised to increase the hassle of air travel and extend the "car rally"?

Labor

Many in the service sector across attractions, lodging and restaurants have left the workforce. They are pursuing jobs in other industries or the gig economy and some, as part of a massive immigrant labor pool, have left the economy all together. Combine this with the fact that visa approvals reached all-time lows during the Trump administration and global border closings have changed immigration patterns around the world, and you have a recipe for a labor shortage. Unionization has also created some challenges for operators and all of this together could mean travel providers struggle to staff enough trained workers as demand increases.

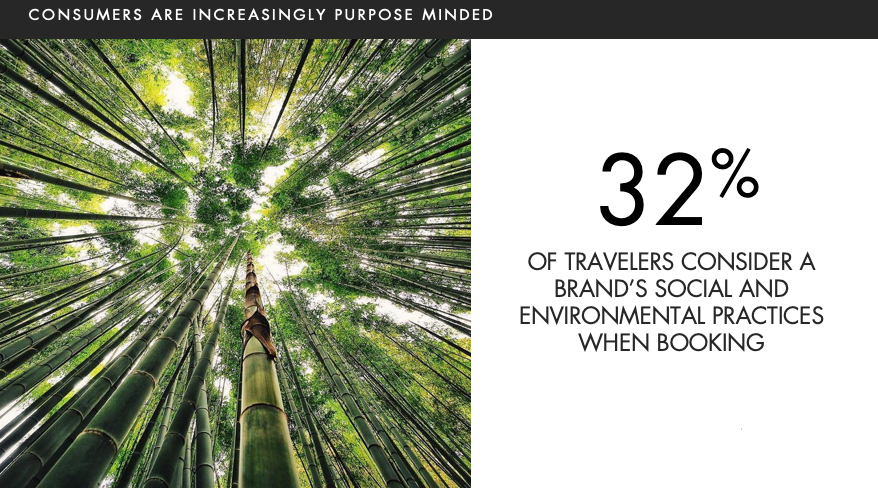

Green and Clean

In our data, travelers now expect brands to provide both safety around COVID-19 as well as an environmental ethos. Alternative energy, carbon offsets and reduced waste are all cited in our research as important to travelers. At the same time, clean protocols and the heightened expectation for safety standards are creating a much larger need for disposables. The cost and policy for these realities are a challenge that will become more pronounced in 2021.

Government and Political Policy

Which airlines will be propped up through Government intervention? Will US states receive federal funding that can be appropriated for tourism efforts? Can small operators in hotel and restaurant categories make it with small business loans or more stimulus? Is Brexit really happening or not? Our best guess is that many small operators will fail in early 2021 and that more than one airline will disappear. But we also believe that the success of tourism policy around the world, as well as the leadership of organizations such as US Travel, WTTC and the ETC, make for a heightened appreciation for the role travel must play in recovery. As a result, we expect government to be additive to travel more than a hurdle and that private markets will look to invest in our industry (ie witness the extremely successful IPO of Airbnb). Programs such as the U.S. EDA grants or the $17 billion of stimulus passed in Australia are hopeful signs.

Some Predictions

- A company you've never heard of will become a major player in AI-driven travel bookings

- Q3 2021 will record the largest travel Q-O-Q volume increase since 9/11

- A majority of big players in air, cruise, lodging and transportation will be profitable in 2021

- Amazon will use the recovery cycle to enter the travel industry in a dramatic way, possibly in concert with a major travel acquisition

- One global airline and one major OTA will disappear or be merged

- There will be another major hotel brand merger

- Microsoft and/or Google will rollout a personal travel concierge app in the U.S. and Europe, in part to respond to more aggressive EU regulators

- Cancellation and change fees will return for airline bookings. Hotels will begin to enforce similar policies

- Travelers will seek more purpose-led, tour-packages to destinations not traditionally in the rotation - think the Arctic, small Mediterranean & Asian islands and off-the-beaten path wildlife locales. By 2024, these experiences may even be in space via Elon Musk & SpaceX.

- RV sales will continue to set records, with 500,000 units sold in 2021, in a nod to the continuation of the great road trip

Always interested to hear feedback so please send me a note or post your thoughts. I'm sure we are all eager to move on to 2021 knowing that the travel industry will be a leading economic boost around the world.